As you learn to save and become more aware of your personal finances, you will find yourself accessing your checking, savings, credit cards and other accounts online or via your mobile phone.

This means bookmarking your banks URLs, installing their mobile apps on your phone, and inevitably the hassle of remembering all of your logins and passwords.

While it is extremely important that you monitor your finances online, it is also important that you are careful and that you safeguard your private information and report any suspicious activity.

Click on the image below to learn 10 Important Online and Mobile Security Tips to follow.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Once you get in the habit of saving money each month, the next question is where exactly to you put the money you are saving?

The obvious choices are to keep it in cash in your piggy bank at home or put it in a bank account.

Well here is a secret… Instead of keeping your cash stashed in your piggy bank, you might as well have the bank PAY YOU INTEREST on your savings balance.

Consider the following quote from Albert Einstein…

The bank will give you several options that pay you interest. Generally the quick options are to open a Savings Account or to put your cash in a Certificate of Deposit (CD).

Click on the image below to learn the pros and cons of each.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

We have all heard the saying from Benjamin Franklin that “a penny saved is a penny earned.”

But it seems that it is just so much easier to SPEND money than it is to SAVE money.

So how do we get started saving money?

Ahh….. That is the hard part…….getting started.

Click on the image below to read a great article that gives you 8 key points to help you start saving money immediately, to help you establish short-term and long-term goals, and to help you pick the right tools to save.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

At some point in your life you might find yourself in a situation where you need some cash quickly.

For example, you might have a doctor bill you need to pay. Or you might need to get your car repaired so you can get to work or you might have a rent bill or a tuition bill coming due.

If you don’t have any savings in an emergency fund, what would you do?

It is a situation that you hope you never find yourself in, but inevitably most of us do.

Click on the image below to read a great article that summarizes your choices, and the risk associated with each of those choices.

Pay attention to the left hand column that shows the progression from the “Lower Risk” to “Higher Risk” choices. A short Pop Quiz follows below the article.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Congratulations on playing our financial life simulation and completing all of our lessons. We now invite you to make the transition from the simulation accounts to real world accounts…

Where are you on your financial journey?

We’re ready to give you personalized, face to face guidance in a safe environment* at a time and location that works for you. Our specialists can help you with more education and resources. We’re just a click away…

You can speak to a specialist at a time that works for you…

or save this page as a Favorite so you can review it later.

If you want to learn more about finances, technology and tools to help you where you are in your journey, we have a dedicated student resource page for you. Visit the student resource page by clicking here.

*Our top priority is to ensure the health and safety of our teammates and clients at each location. We have taken proactive steps to enhance cleaning procedures to limit the risk of exposure, based on guidelines from the Centers for Disease Control (CDC), and follow local restrictions on the number of clients that can enter at one time.

Whether we like it or not, April 15 comes every year and that means our Federal taxes are due.

The average taxpayer spends over 10 hours preparing their taxes.

To reduce the burden of getting organized and preparing your taxes, it is important to stay organized and know what documents and forms you will need to collect throughout the year.

Click on the image below to review the forms and documentation you will need to make the process go as smoothly as possible.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Congratulations! You will soon be graduating from college and negotiating your various job offers.

You have worked hard to graduate and you deserve a great paying job.

But as you start to negotiate your offers, keep in mind that you really should be considering the overall compensation package. Salary is important, but so are things like location and commute to work, your health insurance costs, your retirement plan, and many other benefits that are being offered these days.

Click on the image below to review 9 different benefits that you should consider when selecting a job offer.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

A survey of the Class of 2019 showed that 69% had some form of a student loan.

While most student loans require you to start making payments within 6 months of graduation, there are certain instances where you can defer these payments.

Click on the image below to watch a brief video that explains the difference between loan deferment and loan forbearance. Even if you don’t have a student loan, it is important to understand the difference as it applies to most loans in general.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

If you have done your “rent a house” vs. “buy a house” analysis and you have decided to buy a house, your next thought should be “how much can I afford to borrow to buy my house?”

The answer is easy—it depends! 🙂

It depends on a lot of factors, so click on the image below so you can learn what factors impact how much you can borrow and how big of a monthly mortgage payment you could afford.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Once you have settled down after college and decided where you plan to live for a few years, you will be faced with the question: Should I continue renting or should I buy a house?

While there can be lots of pride in home ownership, it is not without hits drawbacks.

The following video walks you through the benefits and drawbacks of each option.

Click on the video image below to watch the short video.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Did you know that with most credit cards, if you pay the minimum required monthly payment you will end up paying more in interest than what you paid for your original purchase?

THAT is exactly how banks make money and that is why the retail industry promotes the use of bank credit cards and company-branded credit cards.

It is the power of compound interest. If you are investing your money, compounding works in your favor, but if you are borrowing money, compounding works against you.

Click on the video image below to learn how paying just a few dollars more a month on your debts makes such a big difference.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

It seems like a Catch-22. How can you start building your credit if you don’t have any credit to start with?

Well the truth is most banks will give college students and young adults a credit card with a very low credit limit. Then, if payments are made on time for the first few months, the bank will raise your credit limit and then you will be well on your way to building credit.

This helps you build your credit history which then helps to raise your credit score which then helps to lower the interest rate you will be charged on other loans you might get.

Click on the image below of the video to learn how to build your credit from scratch.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Once you have established credit with a bank or credit card company, it is important that you continue to build your credit history and that you keep it healthy.

Click on the video image below to reveal 5 things you can do to help build a healthy credit score and avoid common mistakes.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Most studies show that over 70% of Americans own at least one credit card and carry it with them when they go shopping.

Other studies show that most Americans carry an average balance of $6,200 on their cards and pay interest every month, but they DON’T know what the interest rate is that they are being charged.

Nor do they understand how their payment plan impacts their credit score.

Click on the image below to reveal 7 FACTS that you should know about using credit cards.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

The first question you have to ask yourself when you are thinking of making a purchase is: “Do I NEED this or do I just WANT it?”

Stopping at your local coffee shop every day and spending $2.70 for coffee for 270 days a year adds up to $729 a year. And that’s not counting the gas and the time you take to drive to get that cup of coffee.

Saving money is easier than you think and you will learn from this video how to get started and you will see how quickly it starts to add up.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Everyone needs to take a vacation every now and then.

Or at least travel to visit family and friends.

But for most people who aren’t full-time sales people who travel every week, travelling can be an expensive ordeal.

The good news is that it doesn’t have to be. If you know some of the secrets of airline and hotel pricing, you might be able to save up to 40% on airfare and/or hotels.

Click on the image below to reveal 5 money savings tips when you travel.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Here is one of the most common questions that people who are trying to get control over their finances ask: If I have a little extra cash, do I pay down debt or do I put the money in my savings account?

On one hand financial advisors tell us to stop paying high interest rates on our credit card balance.

But on the other hand they also tell us to make sure we have at least 3 to 6 months cash in our savings account (Emergency Fund).

So which is it?

The answer is easy, kind of.

Click on the image below to review 5 questions that will help you decided if you should pay down debt or save.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Over time, our society moved away from paying for goods and services with gold and silver to paying for things with cash. In the last two decades, we have been transitioning from paying for things with cash to credit and debit cards.

While these 2 cards may look the same, their features and uses are very different.

Knowing the differences between them and knowing when to use them appropriately is an important part of personal banking.

Did you know using one builds up your credit score and the other doesn’t?

Did you know if someone steals your card you may have liability on one card but not the other?

Click on the image below to learn the differences between credit and debit cards in terms of how they work, how they affect your finances, and the inherent security of each.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Hopefully by now you have a real checking account that you use to manage your monthly cash inflows and outflows.

But are you really using all the features that your checking account offers?

While there are lots of negatives associated with a checking account, likes ATM fees and overdraft charges, there are lots of really good features that they offer.

Are you using direct deposit for your paychecks?

Are you able to move money easily between your checking and your savings account?

Do you get alerts when your balances are low?

Click on the image below to review these 8 Tips to Get the Most Out of Your Checking Account.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Now that you are getting used to managing your checking, savings and credit card accounts as part of this virtual platform, it is time you think about opening real banking accounts.

But where do you begin?

What questions do you need to ask a bank to make sure you are getting the right accounts for you?

Click on the image below to learn about the 10 Questions To Ask A Bank When Opening a New Account.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

As you learn to save, become more aware of your personal finances, you will find yourself accessing your checking, savings, and credit card accounts more and more.

While most banks and credit card companies are willing to open up accounts for you for free, keep in mind that every company has to make money some how. So be aware of the various fees that your bank might charge you.

The common fees are usually when you do something wrong, like bounce a check or use the ATM too many times in a month.

But beware of other fees for just using some services that you assumed were free.

Click on the image below to learn about 7 Common Bank Fees.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

As you learn to save and become more aware of your personal finances, you will find yourself accessing your checking, savings, credit cards and other accounts online or via your mobile phone.

This means bookmarking your banks URLs, installing their mobile apps on your phone, and inevitably the hassle of remembering all of your logins and passwords.

While it is extremely important that you monitor your finances online, it is also important that you are careful and that you safeguard your private information and report any suspicious activity.

Click on the image below to learn 10 Important Online and Mobile Security Tips to follow.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

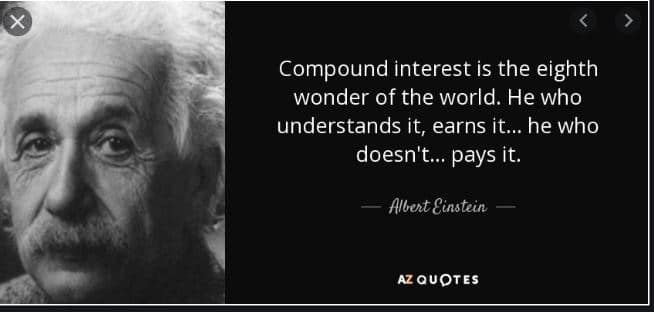

Once you get in the habit of saving money each month, the next question is where exactly to you put the money you are saving?

The obvious choices are to keep it in cash in your piggy bank at home or put it in a bank account.

Well here is a secret… Instead of keeping your cash stashed in your piggy bank, you might as well have the bank PAY YOU INTEREST on your savings balance.

Consider the following quote from Albert Einstein…

The bank will give you several options that pay you interest. Generally the quick options are to open a Savings Account or to put your cash in a Certificate of Deposit (CD).

Click on the image below to learn the pros and cons of each.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

We have all heard the saying from Benjamin Franklin that “a penny saved is a penny earned.”

But it seems that it is just so much easier to SPEND money than it is to SAVE money.

So how do we get started saving money?

Ahh….. That is the hard part…….getting started.

Click on the image below to read a great article that gives you 8 key points to help you start saving money immediately, to help you establish short-term and long-term goals, and to help you pick the right tools to save.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

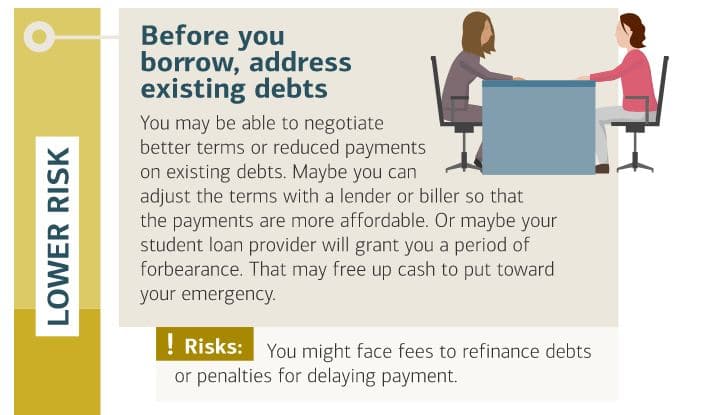

At some point in your life you might find yourself in a situation where you need some cash quickly.

For example, you might have a doctor bill you need to pay. Or you might need to get your car repaired so you can get to work or you might have a rent bill or a tuition bill coming due.

If you don’t have any savings in an emergency fund, what would you do?

It is a situation that you hope you never find yourself in, but inevitably most of us do.

Click on the image below to read a great article that summarizes your choices, and the risk associated with each of those choices.

Pay attention to the left hand column that shows the progression from the “Lower Risk” to “Higher Risk” choices. A short Pop Quiz follows below the article.

This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

PersonalFinanceLab is a gamified platform that focuses on engaging the student through interactive and experiential learning. The platform has a Budgeting game and a stock market platform, that allows the student to learn while doing, making mistakes and repeating the actions until they succeed, thereby learning and understanding the fundamentals of managing money and investing it.

In the last example, I had mentioned Opportunity Cost , which in itself is one of the fundamentals of money management. You have choices that are available to you, whether it be price versus quality or price versus functionality or price versus convenience.

In this edition, I want to discuss the value of money. By this I mean, before you spend your money, you have to recognize it’s worth. For every dollar that is spent, the student has to recognize the value of each dollar in terms of how long it took to earn it and whether the purchase made is the best “value” of your time.

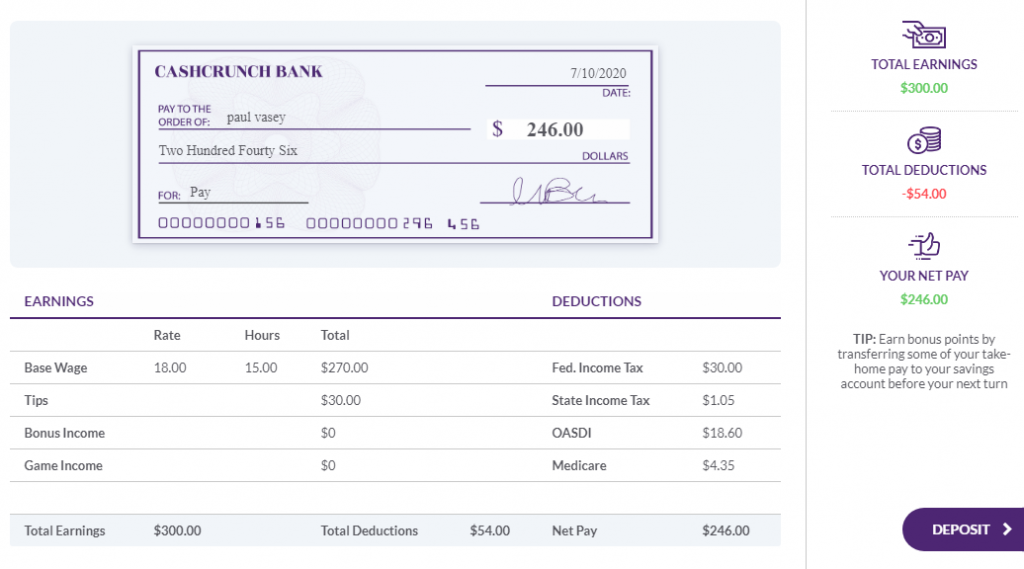

In the Budgeting game the student will receive a paycheck every Friday. In this example, the student is paid $15 an hour, but after taxes they receive $246, which equates to $13.67 an hour.

Now for every purchase, when a student buys a product, they need to be thinking that for every $13.67 spent on bills or random products, it will take 1 hour of their time to earn that money. So if a student wants to buy a pair of sunglasses for $50. It would take that student nearly 4 hours to earn enough money to buy those sunglasses. Firstly are they worth the time taken to earn that money? What else could they have bought with that money (opportunity cost) and did they get the best price and value for their money (comparison shopping)?

Building on from students receiving a paycheck in the game:

Simple activities:

Print out a US map.

Research the minimum wage in 5 states plus their own and label them on the US map.

Research the state income tax in 5 states plus their own including the highest and lowest levels and label them on the US map.

Explain the difference between Total Earnings (sometimes called Gross Pay) and Net Pay.

List 5 thing that you would like to buy or have bought. Using the minimum wage in your state, calculate how many hours it would take you to earn enough money to purchase those products.

In the next edition we will discuss unlimited wants, limited earnings and how we can manage expectations of earning and spending through a Budget.

Want more examples? Check out our lesson plan library, or book a demo with our team to discuss how PFinLab can be used in your class!

Want to get a walkthrough of PFinLab, but no time to schedule a demo with our team? No problem! This recording walks through all the essential features that can help transform your classroom!

For a deeper dive into how PFinLab can be used in your classes, also check out our library of customizable lesson plans, with tons of class project ideas on how you can use our resources in your class!

Bringing gamification into your classroom By Paul Vasey – Former Business teacher, head of department, external examiner, teacher trainer, author and game designer.

Engagement, experiential learning and differentiation.

Through my years of teaching, I found that the most engaged students were ones that were talking about themselves and learning without really realizing it. To expand on this – I liked to use a lot of activities and discussions to teach the basics of concepts before adding theory and terminology so that there was a fundamental understanding of the topic being covered. I would involve the student by making it about them, whether it was a story or an activity so that they could relate and build.

With the PFinLab platform, we do that. We have 2 games, a budgeting game and a stock market game. Students have direct buy in as their decisions made throughout show consequences, which creates an experience that empowers the student to talk about it. We all want students talking about the things we are trying to teach!

Our Budgeting and Stock Market game can be used as both a supplemental and integrated resource. The philosophy of our games is for the students to learn by doing. The focus of the game is to keep things simple and for the student to learn the fundamentals of money management. This resource is not here to replace you, but merely to become a teaching tool that you can use to introduce or consolidate a topic, so the basics can be understood, while theory and terminology can be scaffolded onto initial understanding.

Over time I will be picking an aspect of the game and giving ideas of how it can be used in the classroom. The aspect will include playing the game, completing an activity to apply knowledge and then answering questions to consolidate knowledge.

Lesson 1: Opportunity Cost and Comparison Shopping

Here is a QuickStart lesson that I like to use with my classes to introduce some of the fundamentals of money with our Budgeting Game. Each lesson will require the player to play at least one “virtual month” in the game which will take approximately 20 mins. Further time can be taken to do research and answer questions. Differentiation can be by outcome.

Activity – Making a decision:

When the game starts, the students will have to make choices. They will need to consider their needs and wants, what the alternatives are (opportunity cost) and is it the best price that they can find. Although they will be focusing on price, it is important to recognize that the price is not always the single factor in making a decision.

Here are some sample questions for your students to consider based on deciding where they want to live. These can be done as a written or verbal (group) exercise.

Questions: Testing Understanding

When renting, why should cost not be the only consideration?

How might the location of an apartment have an influence on the monthly rental price?

What are the advantages and disadvantages of sharing an apartment with other people?

Using a realtor website such as Zillow and Realtor.com, find 3 rental properties that you would like to live in and compare pricing, proximity to college and other amenities.

If you are sharing an apartment with others, why is it important to set ground rules?

I hope you enjoy teaching this lesson as much as I do.

Keep an eye out for another lesson shortly. Any feedback, ideas or requests for lessons on topics, let us know!

PersonalFinaceLab’s curriculum library is packed full of automatically-graded quizzes and assessments at the end of every lesson. However, to give students an additional push, you may also want to assign students open-ended questions for short written assignments, or launching points for class discussion.

Most of our Personal Finance lessons end with 4-6 “Challenge Questions” – you can find a list of all questions here.

What is the difference between a secured and unsecured loan?

Using the internet, type in mortgage and research what types of mortgages and borrowing rates that are being made available to the public.( Do not submit an application) Provide examples for each type.

What are the advantages and disadvantages of buying or renting a house?

How might budgeting help parents with being able to afford to raise a child?

How does your expense structure change with the different ages and stages of raising a child?

Other than the actual cost of paying to raise a child, what other non financial factors should also be considered in raising a child?

Are there any programs are out there, both government and private that are there to assist families and children in times of financial and emotional need?

What assets do you currently own? How could those assets help you accumulate wealth for your future?

Setting goals to build wealth are truly key to helping you have a successful, happy future. You don’t have to be filthy rich. You just need enough money to support the lifestyle you’d like to live. Thinking about your future, what is one financial goal you’d like to have for yourself in your 20’s? What choices would help you reach that goal? (Students could choose from a goal for their 20’s, 30’s, 40’s, etc.)

As technology continues to evolve in our society, it is possible that the way we store our money and pay for transactions will change. What do you think that process might look like 15 years from now?

What additional security measures do you see happening in the future in order to keep scammers from fraudulently stealing people’s money?

Describe your experience with using the different financial tools you learned about in this lesson.

Based on your current income (or future) income from a part-time job while in high school, explain which financial institution would be the best fit for you. Include at least three reasons why you would make that choice.

Your uncle wants to start his own business but needs to borrow money in order to do that. What advice would you give him about the type of financial institution most likely to work with him?

You have your first part-time job and are working 20 hours per week. Your parents have asked you to be responsible for paying for your cell phone bill, your car insurance, and for putting gas in the car. They would also like you to start saving for college expenses. Explain how you would use a savings account and a checking account to help manage your finances.

List 3 National Banks, 3 Credit Unions and 3 Savings and Loan Institutions near your home.

Our latest teacher webinar walks through some of the basics of gamification – and the keys to best leverage these new levels of engagement to supercharge your blended and remote classrooms this Fall!

If you are using a blended or fully-remote classroom, quality online resources are more important than ever! Our new Badges and Achievement update to encourage exploration, and Rewards to incentivize students to complete their classwork on time, we are excited to work with your classes this Fall!

[contact-form-7 id=”17909″ title=”Pfinlab Order Form”]

With the next major update to the PersonalFinanceLab Budget Game, your students can graduate from school and start their Full Time Jobs!

How It Works

If you have used the Budget Game before, your class would have taken on the role of college students with a part-time job. They would be working variable hours each week, and have had roommates to keep their bill costs down.

With the new Full Time Mode, your students will take on the role of a freshly-graduated student who just started their first full-time job. From a student’s perspective, the new additions include:

Consistent Hours – students will always work 40 hours per week for bigger, and more consistent, paychecks.

New Bills – full time workers now have to make Health Insurance and Student Loan payments. These bills come up near the start of each month, and students need to be careful on how they prioritize their bills to make sure they can always hit their savings goals!

More Expenses – students no longer have roommates, which means their rent and utility bills go up substantially.

Professional Development – instead of “studying”, students have the option to conduct “Professional Development” on the weekends to build new skills useful for their job. If they build enough new skills, they can earn a raise at their job!

New Events – the “life events” throughout the game also get updated once students enter the workforce, with dozens of new (and often very expensive) events coming into play.

Graduation

With this update, your class can get the best of both worlds. Teachers can have their class start the game in the “part-time mode”, where they act as a college student with a part time job. As the teacher, you can say that every student “Graduates” into the full-time workforce after a certain amount of time.

A typical class would have the students start out with a part-time job, graduate after 6 or 12 months, and continue as a full-time worker for an additional 6 or 12 months, as your class time allows.

Transition to Full Time

When a student graduates, they are given a “Congratulations” screen, and informed that they are transitioning to the full time workforce. Key elements of the transition period include:

Students need to move out of their old place and to a new part of the city. They will have to pay fees to break their old lease, and choose new options for their bills.

Extra time students spend “studying” as a student count towards “Professional Development” when they start their job. If they studied hard, they might start their full-time job with a bigger salary than the rest of the class!

New thresholds are added for their Emergency Fund. Saving an additional $1500, $2000, and $5000 will earn students even more points.

Their credit score, quality of life score, and savings bonus points all carry over – every action taken as a student can impact their new life as a worker!

Behind The Curtin

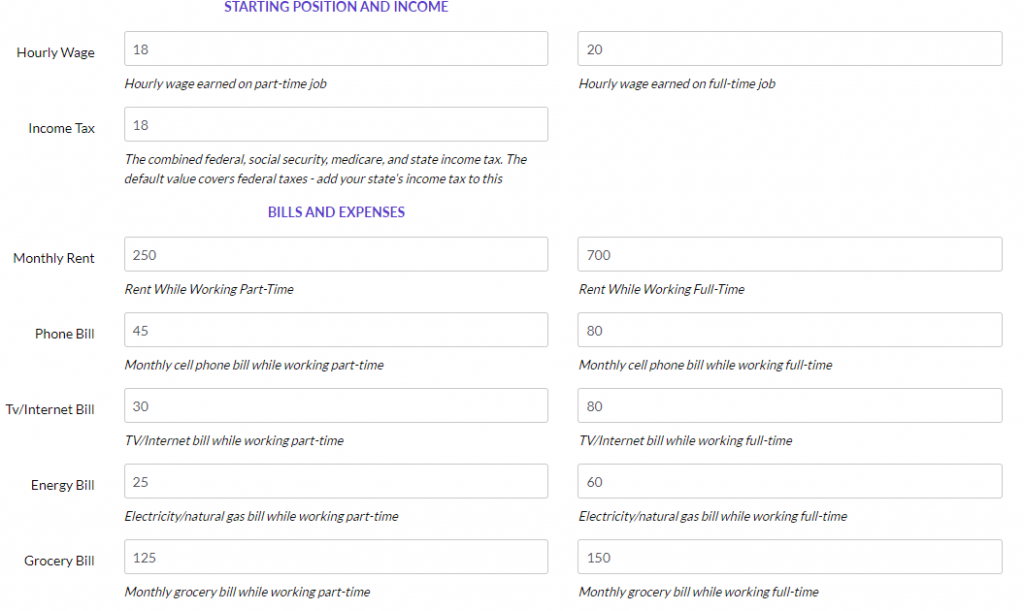

As the teacher, you still have complete control over your class, so you can tweak all settings to reflect your town or city’s reality. You can separately set the wages and “base” bill amounts for everything, both for while students have their part-time job and full-time job.

But don’t worry – we have default settings that work well for almost every class!

As the teacher, you have complete control of your class’s game modes. You can have students start immediately with their full-time job (skipping the “college student” phase entirely), include the transition period of Graduation, or continue to use the Part-Time mode only, depending on the objectives for your class.

All together, this makes the Personal Finance Lab Budget Game the most realistic and engaging way to teach your class how to manage their money and prepare for the road ahead! If you don’t have a license for PersonalFinanceLab yet, or need a renewal, request a quote with the form below!

[contact-form-7 id=”17909″ title=”Pfinlab Order Form”]

This Summer, PersonalFinanceLab has partnered with BountyBlok to power our awesome new Badges and Achievement system to bring classroom engagement to a whole new level!

Personal Finance should never be boring for students – by working with BountyBlok, our Assignments engine is supercharged with new ways to track student activity and provide them with real-time rewards.

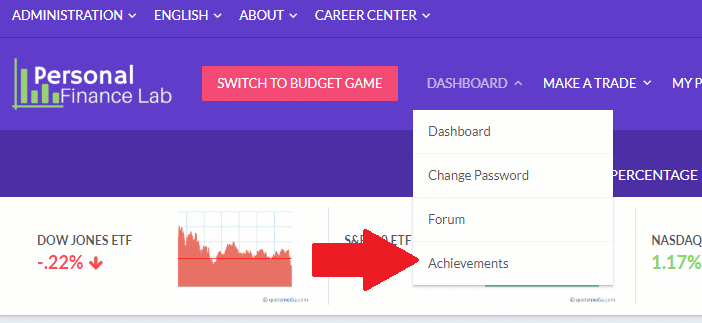

With your next class, your students will have an “Achievements” option on their menu under “Dashboard”:

This new page shows a list of achievements they can achieve, along with their current accomplishments.

Students can earn achievements by completing actions throughout the Stock Game, Budget Game, and Curriculum library. Completing each achievement earns the student a badge they can show off on the rankings page too! Once a student earns a badge, clicking it makes it “Active”, and appears throughout the site as their new avatar.

If a student clicks another students’ badge on the Rankings Page, they will get a list of all the other badges earned – a great way to “show off”!

Badges are “Leveled Up” as students improve their mastery of a topic or subject. Higher level badges are harder to get (with fancier colors and effects), and students will usually need to complete new challenges at a higher level than your class requirements to achieve full mastery!

Our new Badge system gives students a great way to differentiate themselves in the class rankings while also encouraging every student to go “Above and Beyond”, learning to explore new concepts beyond the base requirements for every class. However, if you do not want to utilize Badges for your class, you can also turn them off in your class settings.

If you don’t have a PersonalFinanceLab license yet, or need a renewal, request a quote for your class with the form below!

[contact-form-7 id=”17909″ title=”Pfinlab Order Form”]

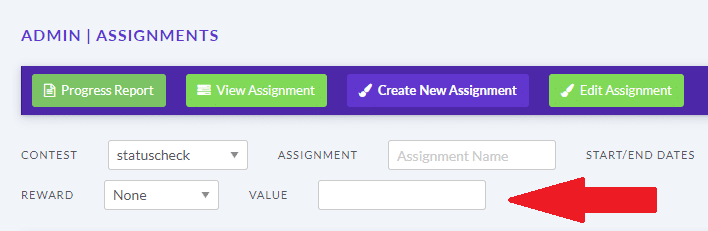

Our first major enhancement of the summer is almost here! The next release of Personal Finance Lab focuses on our Assignments – our awesome system used to manage curriculum and track your students’ progress through our Stock Game and Budget Game. There’s three game-changing new features you can expect for your next classes: Rewards, Prerequisites, and Content!

Rewards: Instant Cash Bonuses!

The next time you set up your class Assignment, you’ll notice a new option – “Rewards”:

This is a brand-new way to make sure your students complete their work on time!

A “Reward” is a cash bonus that your students receive when completing the assignment. You can choose whether the rewards are applied to their Stock Game portfolio (it appears as extra cash added to their account), or their Budget Game checking account (it gets direct deposited).

This means students who finish their assignments get an instant boost in the Class Rankings – the perfect incentive to get their work done on time!

Prerequisites: Self-Paced Learning!

You might also notice another option when you’re creating your assignments – “Prerequisite”:

For the first Assignment you create for your class, this will be empty. This new tool will let you “queue” assignments for your students to let them learn entirely at their own pace.

By setting a “Prerequisite”, students will need to complete one assignment before they can progress to the next. As soon as students complete the “Prerequisite”, students are prompted to continue to the next set of lessons and activities, letting them move at their own pace.

Typical Use Case

As a teacher, I want to set up activities for my students every week, and I want to make sure everyone completes everything in a certain order. However, I know that some students might take longer than others.

I would:

Set up my first assignment (“Week 1”), with a “Start Date” of today, with the first set of activities

Set up my second assignment (“Week 2”), with a “Start Date” of a week from today, with the second set of assignments. I would set my “Week 1” assignment as a prerequisite.

For my students, everyone starts today and start work on the “Week 1” assignment. Next week, students who finished the first assignment are prompted to begin the “Week 2” assignment.

BUT students who have not yet finished the “Week 1” assignment need to complete that first. As soon as they do, the Week 2 assignment pops up for them to start too.

Combining “Start Dates”, “Due Dates”, and “Prerequisites” give teachers a whole new toolkit for giving students pacing and structure to their experience throughout PFinLab!

Curriculum Update

We are also rolling out an update to our entire Personal Finance curriculum! We’ve been working hard with a team of dedicated educators from around the country to conduct a full audit of our lessons and assessments to make sure they are the best they can be. The topic list will have minor updates, but the contents of every lesson has been reviewed, updated, and revised for 2020.

There’s a lot more coming where that came from – with new updates coming throughout the Summer! If you already have a Personal Finance Lab license for your school, set up your Fall classes today. If you don’t have a license yet, or need a renewal, request a quote for your class with the form below!

[contact-form-7 id=”17909″ title=”Pfinlab Order Form”]

Teachers Have Already Claimed Over

$250,000 of Student Accounts of PersonalFinanceLab.com’s Personal Budget Game

and Stock Market Game.

For

Immediate Release

(Montreal, Quebec) April 24, 2020 – In response to

teacher and parent demand for its online educational services, Stock-Trak Inc.,

the leading provider of educational personal finance games, is now offering

access to its PersonalFinanceLab.com site for free to teachers, parents and

their students for the balance of the 2019-2020 school year.

PersonalFinanceLab.com offers a variety of personal

budgeting games and stock market games, each with its own set of curricula. In

addition, Stock-Trak is donating prizes to the top students nationally that

complete the games and the required lessons.

“Once we realized that both teachers and parents were in

desperate need of online educational resources for their students and children,

we decided to create some national competitions and offer free access to our

PersonalFinanceLab.com site. The response has been overwhelming and we have now

given away over $250,000 of student accounts,” says Mark Brookshire, Founder

and CEO of Stock-Trak Inc, the company that owns PersonalFinanceLab.com. “As long as there is demand, we will continue

to grant free access through June 30, 2020,” he added.

The personal budgeting game allows students to create a

monthly budget of income and expense items. Then students manage the day to day

activities of paying bills, deciding whether to pay cash or charge items,

making decisions on payment plans and insurance, managing their credit card

balance and credit score, and many more financial literacy topics.

The stock market game gives students a virtual $100,000 and

the accompanying lessons help students understand how to build a diversified

portfolio.

About Stock-Trak Inc.

Stock-Trak offers a variety of virtual trading and personal

finance applications for both the academic and corporate markets. Our family

of virtual trading and stock market education sites (StockTrak.com,

PersonalFinanceLab.com, HowTheMarketWorks.com, WallStreetSurvivor.com,

and Investinig101.net) helps over 800,000

students and adults each year learn how the stock market works and become

more confident in their investing decisions. Our robust virtual

trading platform can also be customized to meet the needs of banks, brokerages,

media companies, and other financial websites to enable them to offer their

clients a virtual stock trading experience. Founded in 1990,

our virtual trading platforms and websites have helped over 8,000,000

individuals learn about the markets and practice their trading skills.

Contact:

Mark

Brookshire at (770) 337-7720 Mark@StockTrak.com

If you find yourself teaching a class remotely for the first time this Spring, never fear! PersonalFinanceLab.com has everything you need for a knock-out distance learning class, all in one place. Our engaging simulations, interactive games, built-in assessments, multi-media curriculum, customizable lesson plans, and teacher presentation and video library has everything you need to turn this semester into a smashing success.

If you’re using our resources for the first time, this guide will have everything you need to get off to a running start in less than 5 minutes!

Step 1: Set Up Your Games

PersonalFinanceLab centers our resources on our Stock Market and Budgeting Games. Both games are highly customizable, and will keep students fully engaged and focused on the class. The first step in having a successful online course is to set up these foundational activities – and our support team will be with you every step of the way!

You can use one game or the other, but using both is the best way to get the most engagement out of your class!

The Budget Game

In the Budget Game, students taken on the role of a college student with a part time job – they will need to manage their variable income, unexpected expenses, and tough decisions as they work to improve their Net Worth, Credit Score, and Quality of Life. Students progress through time (each “month” taking about 20 minutes), with each decision having long-lasting impacts on how the game plays out.

Teachers can control the types of life events that occur in-game, along with what bills students receive, how much they earn at their job, and much more. You can even give them “shocks” by increasing their rent or other bills mid-game! Students can also see their performance against other students in the class by Credit Score, Quality of Life, Net Worth, or their overall Game Score.

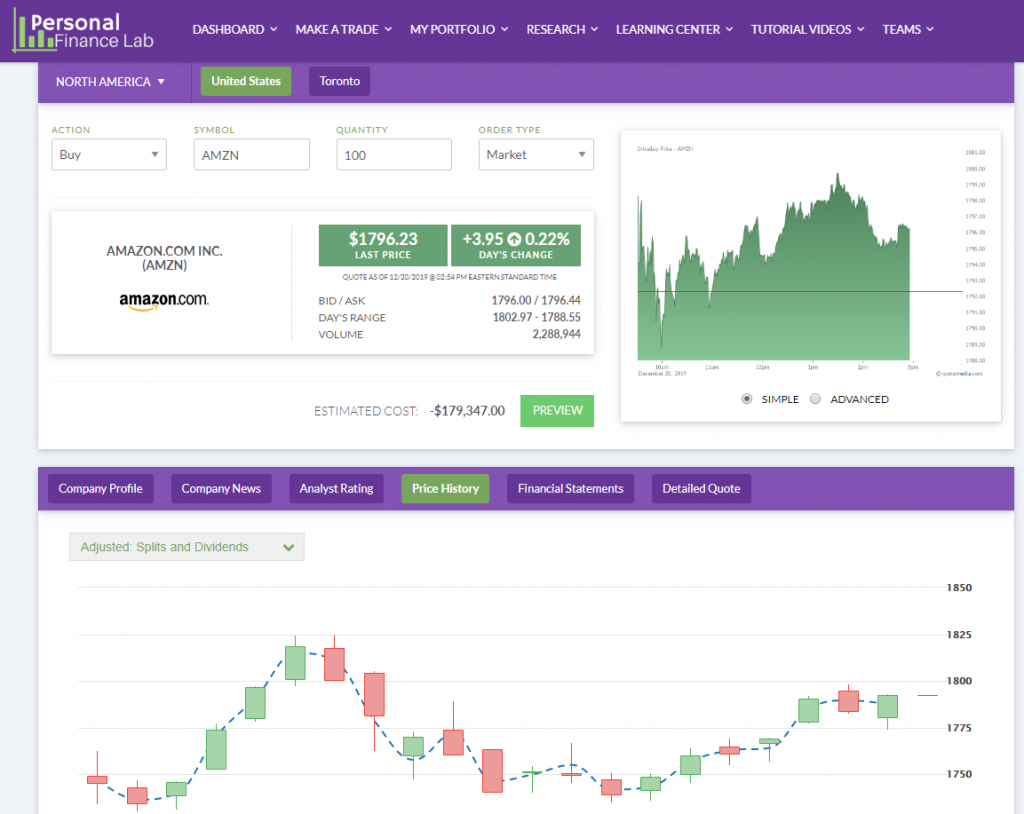

The Stock Game

Our real-time stock game brings investing education to a whole new level. Students buy and sell stocks, mutual funds, and bonds at real-time prices, and can track their performance with real-time class rankings. Students take notes with every trade to explain their rationale. Teachers can group their students together into Teams to build a shared portfolio for an excellent group project.

All research is built right in, with quotes, charts, analyst ratings, and much more put right at your student’s fingertips (along with plenty of help and tutorials to help them get moving!). There are tons of teacher reports showing all student activities, and lots of teacher help to show how to get investing conversations started in class.

Step 2: Pick Your Lesson Plans

Next up, you’ll take a stroll through our comprehensive, customizable lesson plan library. Each lesson plan overs a specific Personal Finance topic, like Credit or Investing.

We then break down 7-15 activities specifically optimized for distance learning: specific prompts for how students should approach their budget game or stock game, lessons from our mixed-media Curriculum Library, pre-built Google Slides and PowerPoint presentations that you can use for direct instruction, class discussion points you can use as prompts on your LMS, and more.

Each activity shows an approximate time for completion, pick and choose the activities – everything you need to give an awesome distance learning experience, all in one place!

Now that your games are set up and you’ve chosen the lesson plans you want to use, set up “Assignments” for your class on PersonalFinanceLab.com. Assignments are list of tasks and lessons you assign to your students – our curriculum library has over 300 lessons aligned to state and national standards that you can integrate with your class with a click of a button.

If you started with the Lesson Plans, it will include several recommended lessons from our curriculum library for each topic, but feel free to mix and match to suit your class.

We use mixed media for our lessons, with a combination of articles, videos, infographics, and interactive activities to bring everything together. Every lesson ends with a short, 3-5 question Pop Quiz Assessment – you can choose whether students can re-take the assessment for a higher score, or if you want to save their first attempt to your Grade Book.

Each Assignment will have a start date and a due date. When your students log into PersonalFinanceLab to check their portfolio in the Stock Game or make more progress in the Budget Game, their Assignment will also appear on the page, listing the lessons they are expected to complete and a countdown for when it is due.

Step 4: Students Compete And Learn!

Now you’re home free! The live rankings from both the Budget Game and Stock Game help keep students engaged, while your Assignments keep students on-task for the course learning objectives. You can use the discussion prompts to encourage further engagement, and review student performance on each Assessment to identify any problem areas.

To get started, you’ll need to order accounts for your class. We cut our normal price of $15 per student down to $5 per student to help out schools forced to go “Remote” for the remainder of the Spring 2020 session – you can either buy accounts directly or request we invoice your school.

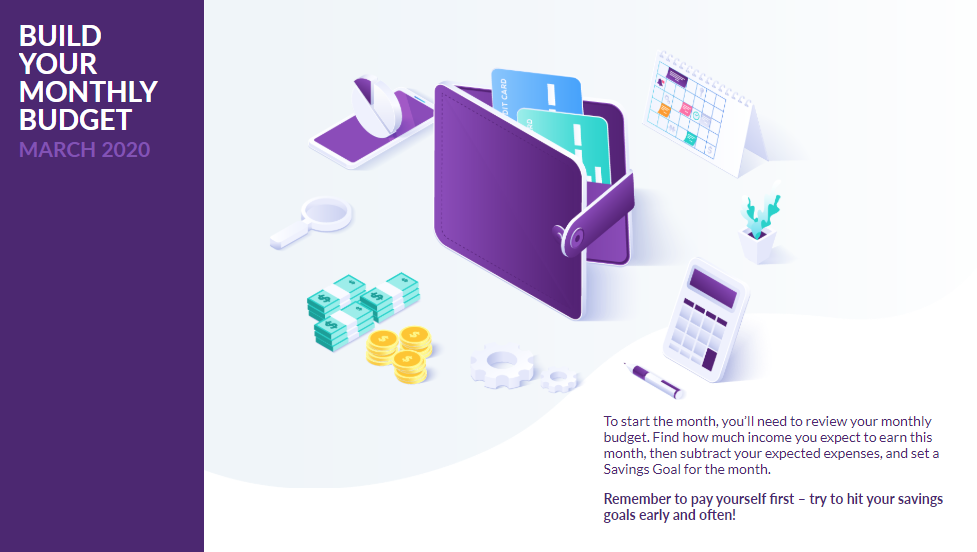

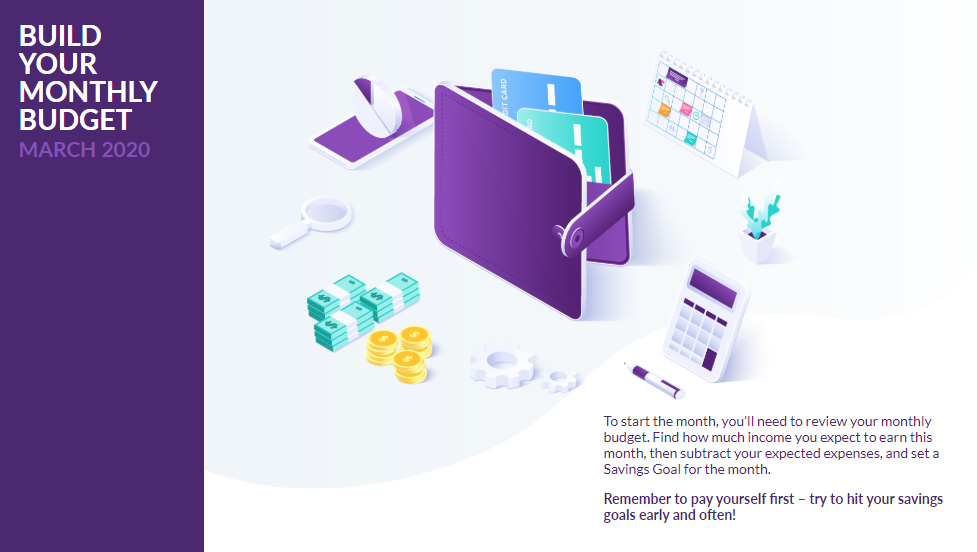

Just in time for March, the Personal Finance Lab team is excited to announce a massive new update for our budgeting game!

Our latest update includes some huge enhancements for your class, including:

An overhaul to the Quality of Life scores, making the point scoring system much easier to understand.

A new Overall Game Score, synthesizing student’s Credit Scores, Quality of Life, and general savings habits into one metric.

A new “Budget Builder” activity each month, where students compare their upcoming income, estimate their expenses, and set savings goals for the month.

A new “Budget Summary” at the end of each month, showing students how well they stuck to their savings goals (and awards bonus points!)

New integrated Tutorials and Lessons that occur regularly throughout the game highlighting key budgeting skills

Quality of Life Update

The key trade-off in our budgeting game (and real life) is the decision to Save or Spend. We capture this in our Quality of Life score, where students can increase their Quality of Life by renting nicer apartments, having better cell phone/internet plans, or buying luxury goods. Our original feedback was that many students were having a hard time understanding this score, so our new update makes things pretty simple:

They will get Quality of Life points for spending and purchases beyond the “Bare Minimum”, plus bonus points for Socializing, Studying, or taking care of their Household Chores.

Points From Spending

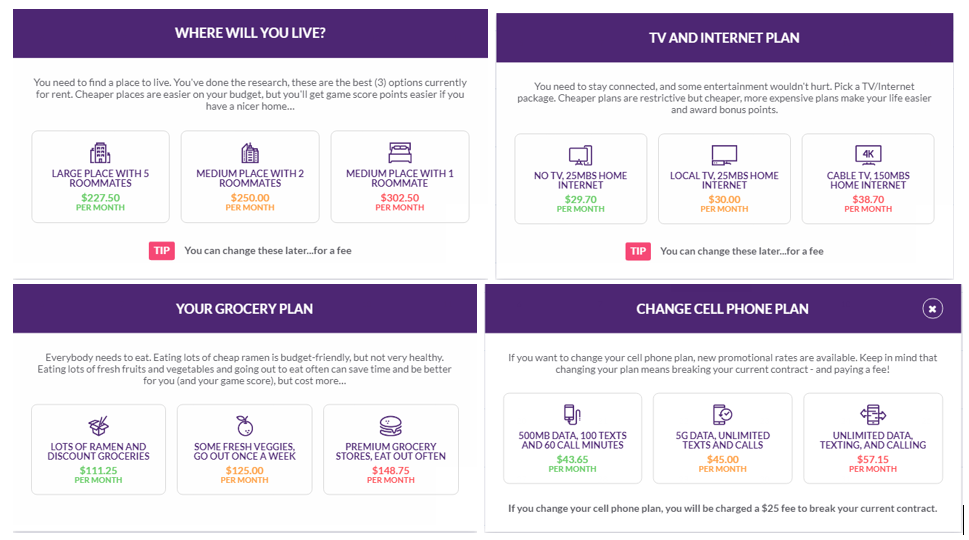

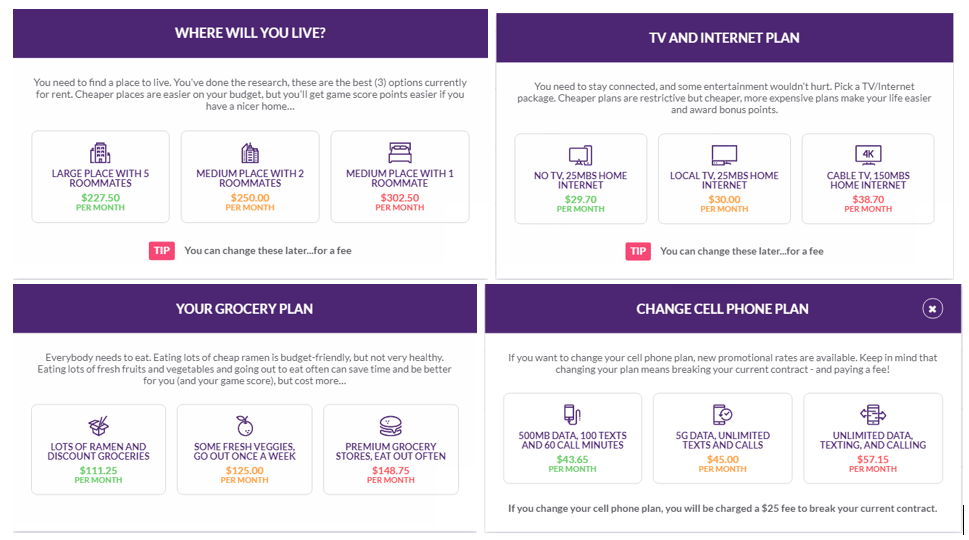

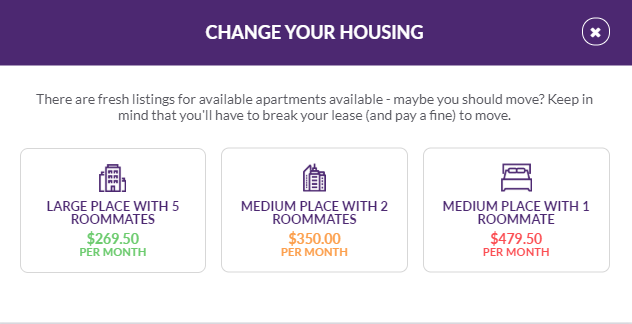

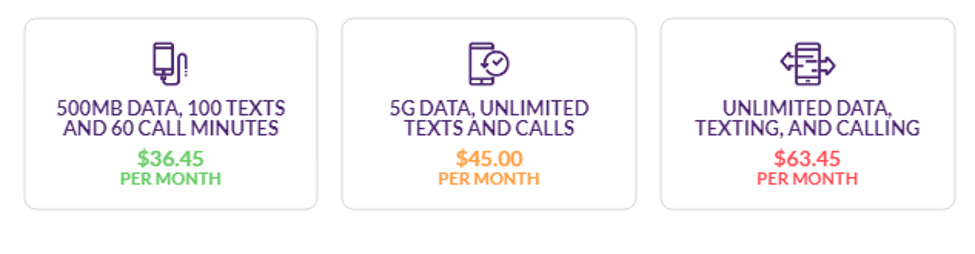

Every month, students make dozens of decisions in the game. But one of the biggest is where live. We give students 3 options when they first join:

In the example above, students who choose the $270 option would earn 0 Quality of Life points, since they are choosing the bare minimum to survive. Students choosing the middle option would earn 80 points each month (350 – 270 = 80), while students choosing the most luxurious option would earn 212 points.

Students have the option to move apartments or change their cell phone/TV plans any time (for a fee), so if they find they can’t quite afford the luxuries, they can scale down (and lose some Quality of Life). The same point system applies for all the other spending choices students face throughout the game – points are earned for luxuries above the bare minimum.

Points from Weekend Choices

Every weekend, students choose how to spend their time – Working to earn more money, Socializing with friends, taking care of Household chores, or Studying.

We now also award 50 Quality of Life points every time they Socialize, and 25 points every time they take care of their Household or Study.

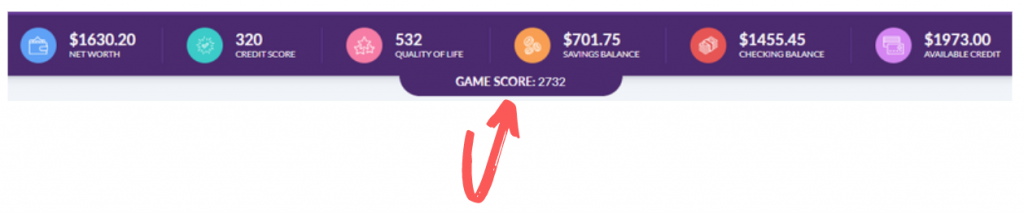

New Game Score

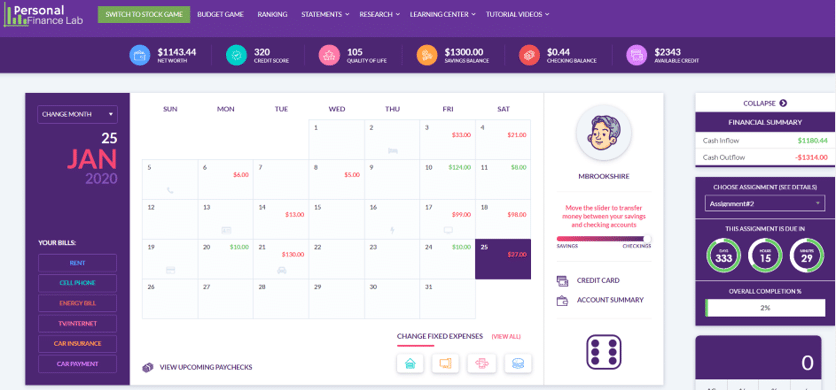

There’s a brand-new Game Score we added to the top of the Budget Game:

The Game Score is a metric on how well students are following Personal Finance best practices. Students maximize their Game Score by making wise personal finance decisions (not just trying to save every penny).

The new Game Score combines the student’s Quality of Life Score, Credit Score, and how well they are reaching their savings goals.

Students earn 1 Game Score point for every Quality of Life point.

Students earn 5 Game Score points for every Credit Score point.

Students earn 1000 Game Score points by funding their Emergency Fund – 1000 points when they put $500 in their savings account, and another 1000 points when they save up a full $1000.

Plus additional Game Score points for hitting monthly savings objectives.

We’ve balanced the Game Score to encourage students to build up their Emergency Fund quickly, always save at least 10% of their income, responsibly use their credit card, but also take care to invest in their Quality of Life (rather than simply always choose the cheapest options for every choice).

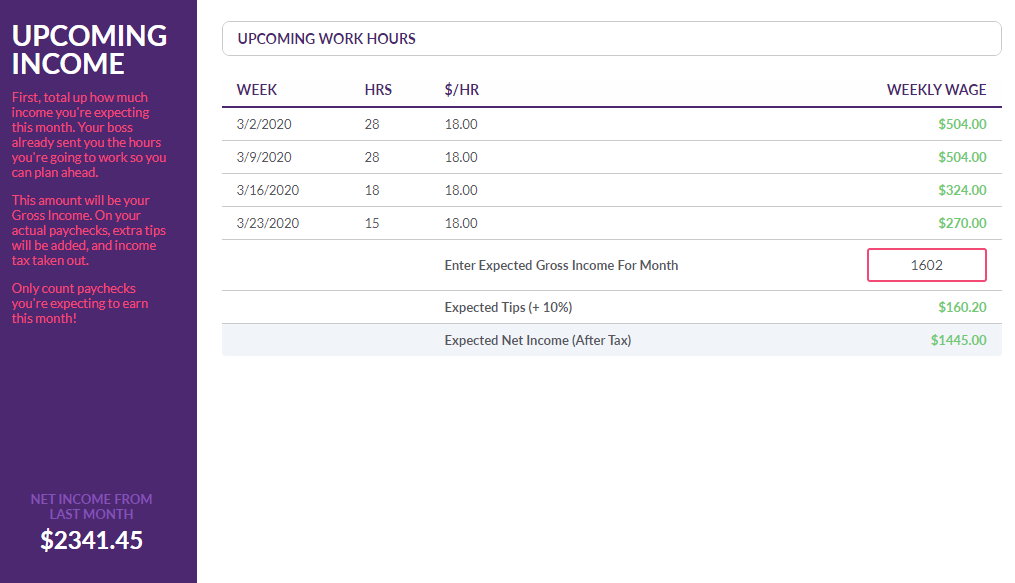

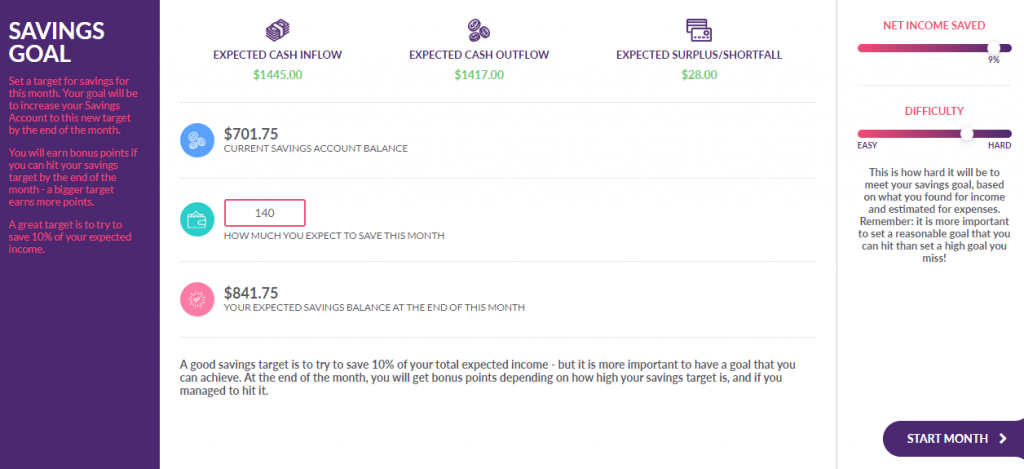

New Budget Builder

At the start of every month, students will now need to complete their Budget Builder – this will ask students to find their expected income for the month, estimate their expected expenses, and set a Savings Goal.

Estimating Income

First, students will see how many hours they are scheduled to work for this month. They need to sum up what they expect as their paychecks, and we give them an estimate for how many “Tips” they will receive, and deduct their income tax. We also show students how much they earned last month, so they can plan ahead if they expect to earn more or less.

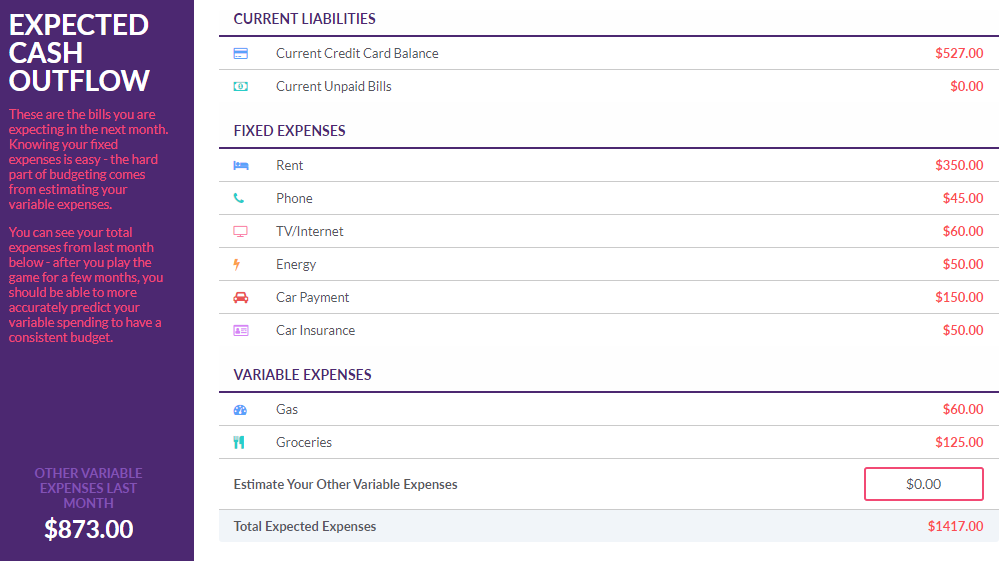

Estimating Expenses

Next, students see their expenses for the upcoming month – plus any unpaid bills and credit card balance they are carrying over from last month. Students need to make a guess as to how much they will spend in “Unexpected Expenses”. The first month of the game this will be a blind guess, but we also show students what they spent last month. This gives students a great way to learn how to estimate their expenses based on their spending history.

Setting Savings Goals

Last, we show students what they found their income and expenses, and ask them to set a Savings Goal for the month. We highly encourage to students to set a Savings Goal of 10% of their income, but it is more important to set a goal they can actually achieve than one they cannot. On the right side of the page, we give them a gauge on the quality of their goal (with 10% being “Great”), and a difficulty level (depending on their expected surplus or shortfall) – giving students a perfect benchmark to temper their spending for the month ahead.

End of the Month

At the end of each month, we also now prompt students with a Monthly Summary, showing how well they hit their savings goals.

Students with a 10% or higher savings goal that hit it will earn an extra 600 Bonus Points to their Game Score.

Students with a 5% or higher savings goal that hit it will earn an extra 300 Bonus Points to their Game Score

Students with very low goals, or who miss their goals, don’t earn any bonus points.

Integrated Lessons and Tutorials

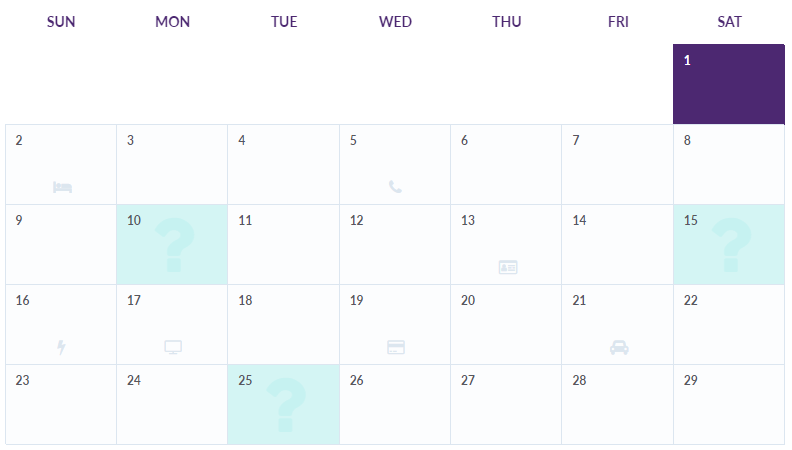

When students start the game, the calendar will look a bit different, with some new Green calendar days:

On these days students will be prompted with a mini-lesson both to illustrate an important Personal Finance concept, and to help them to be successful in the Budgeting Game.

Students need to read the short lesson and complete a Challenge Question to continue. Each mini-lesson takes between 2 and 5 minutes to complete.

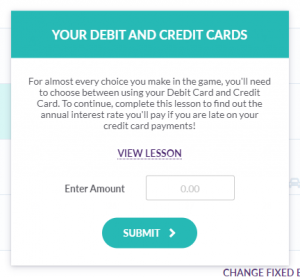

Some of the first lessons include:

The difference between their Debit Card and Credit Card

The importance of an Emergency Fund

How their Credit Card charges interest and fees

How to prioritize their bills if they are short on cash

Students will get the most tutorials right at the start of the game, but a few more appear throughout the session (filing taxes, budgeting for the holidays, and other special events).

We hope your class gets as excited as we are to dive in and get budgeting!

As you may well be aware, we have a Budgeting game which can be used as both a supplemental and integrated resource. The philosophy of the Budgeting game is for the students to learn by doing. The focus of the game is to keep things simple and for the student to learn the fundamentals of money management. This resource is not here to replace you, but merely to become a teaching tool that you can use to introduce or consolidate a topic, so the basics can be understood, while theory and terminology can be scaffolded onto initial understanding.

Here is a QuickStart lesson that I like to use with my classes that you can use with your classes to introduce some of the fundamentals of money with our Budgeting Game. Each lesson will require the player to play at least one “virtual month” in the game which will take approximately 20 mins. Further time can be taken to do research and answer questions. Differentiation can be by outcome .

Lesson: Comparison Shopping

When shopping it is really important to understand that we do have choices. But buying objectives should be noted. With opportunity cost, we are looking at the cost of giving one thing up for another. With comparison shopping, it is the process of finding and then looking at the choices available to us.

Quite often we assume that price is the only thing that we should consider when comparing products. However, along with the initial price saving, will quality actually be a factor? Are the needs we have defined met by that choice? Do you get what you pay for?

It is always important to understand why you are buying that product and how you intend to use it. There are various ways to compare products, including price comparison websites, reviews of products and the part where you actually try things for yourself and make a decision.

This concept follows on nicely from opportunity cost where the student will want something, but will have to forgo other options.

Activity

Within the Budgeting game, students will have many choices to make.

For one round of the Budgeting game, students should find out how much they have paid for their internet, cell phone and groceries. They should then research alternative plans available to them and produce a comparison list. For the internet and cell phone, they could include the price, plan, coverage etc. For the groceries, they should create a list of groceries that they would buy for a week and then compare prices between 3 supermarkets, remembering to look at the price per unit/weight/volume. Encourage the students to discuss the variation in prices they have found and how they can use this method to reach saving targets.

I hope you enjoy teaching this lesson as much as I do.