Stock and bond prices move up and down every day, sometimes by very large amounts. If you want to start investing, the first thing to understand is why these price movements happen, and how to plan for them.

Stock Price Movements

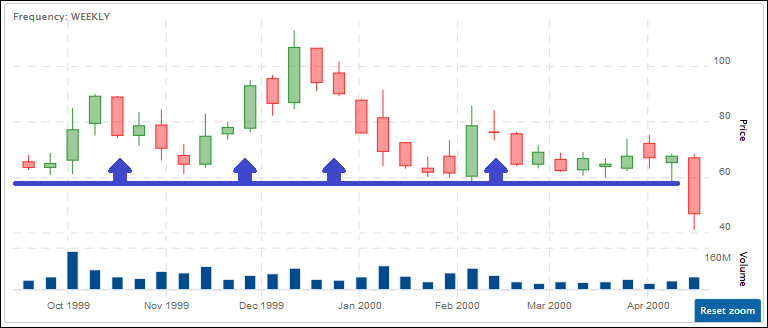

If you look at the stock for any public company you will often see a line graph that depicts how prices change every day. You may see sharp movements in certain stocks while others have smaller shifts. Stock prices are the reflection of the present value of future earnings expectations. The present value of future earnings is divided by the total number of shares that were issued by the company. In other words, the stock price reflects the expected performance of a company at some point in the future.

To see how the process works, start from the beginning: the investment bank that oversees a stock’s IPO.

Investment Banks

Investment banks are multi-tiered corporations that enable companies to have their stock traded on a public market. Examples of famous investment banks include Goldman Sachs GS, JP Morgan JPM, UBS, among others. Any public company you can think of today was once held privately. They used the services of an investment bank to become a publicly traded stock. The process to become publicly traded is known as an initial public offering, or IPO for short. Once a company is listed on a public market anyone can buy, sell, or trade the stocks.

The IPO Process

The process begins with a company discussing the pitch for an IPO with bankers. The company selects book runners and co-managers who will be responsible in selling the newly issued stocks for the primary bank. The company must file the registration forms and discuss the timing of the IPO. The bankers then conduct due diligence, a process by which they speak to customers, do research and analysis on the industry and trends, figure out the legal situation, and sift through the financial statements and make sure there are no irregularities. The S-1 form is filed after the due diligence, which releases the historical financial statements, key data, and other information investors would like to see before making a purchase decision.

The process begins with a company discussing the pitch for an IPO with bankers. The company selects book runners and co-managers who will be responsible in selling the newly issued stocks for the primary bank. The company must file the registration forms and discuss the timing of the IPO. The bankers then conduct due diligence, a process by which they speak to customers, do research and analysis on the industry and trends, figure out the legal situation, and sift through the financial statements and make sure there are no irregularities. The S-1 form is filed after the due diligence, which releases the historical financial statements, key data, and other information investors would like to see before making a purchase decision.

The pre-marketing stage involves bankers speaking to investors regarding the company and industry in order to determine a price range to sell the initial stock offering. The final price will be set after more conversations with investors. Banks will then allocate shares to different investors prior to the first day of trading. Once shares are allocated, investors can now buy, sell, and trade to each other while the general public can begin to purchase shares.

The period following the IPO is often considered the most volatile period in a stock’s history because of investor sentiment. Investor sentiment is how large-scale buyers of stocks feel about companies, industries, and the market as a whole. Investors are typically large financial institutions that employ economists, analysts, and industry experts who drive the appetite of a specific stock or industry.

Investors that are bearish are under the assumption there will be a decline in the stock or market. Bullish investors anticipate growth in a specific stock or the market. Investor sentiment is driven in part due to earnings.

Earnings

After the IPO, a stock’s price movements are dominated by earnings, both realized and expected.

Earnings reports are made available to the public to announce a company’s most recent historical performance. Quarterly reports feature the previous three months, while annual reports provide a snapshot of the most recent year. These reports feature commentary from the company about initiatives and projections moving forward.

The one metric that affects stock prices almost immediately following these announcements is EPS (earnings per share). This represents the portion of the company’s profit that is allocated equally to each outstanding share. Analysts converge to create a consensus estimate regarding the EPS of each company during each quarterly announcement. If the actual EPS is greater than the estimate there is usually a spike in the stock price. If the company misses the estimate there is likely a decrease in stock price. Additionally, within the reports there may be other metrics that investors look at which may also cause a swing in either direction.

Systematic vs Unsystematic Risk

Finally, stock price fluctuations deal with the concept of risk. There are two types of risk, systematic and unsystematic. Systematic risk is an event that can affect the stock market as a whole. Unsystematic risk is specific to the company or industry. Beta is the measure of the volatility a stock has in comparison to the market as a whole. A beta greater than 1 represents a stock that will move higher than the market in periods of growth but decrease more in periods of decline.

Finally, stock price fluctuations deal with the concept of risk. There are two types of risk, systematic and unsystematic. Systematic risk is an event that can affect the stock market as a whole. Unsystematic risk is specific to the company or industry. Beta is the measure of the volatility a stock has in comparison to the market as a whole. A beta greater than 1 represents a stock that will move higher than the market in periods of growth but decrease more in periods of decline.

Systematic Risk

Systematic risk includes events such as wars, interest rate fluctuations, recession, and geopolitical occurrences. These events tend to affect all stocks regardless of company specific performance and growth prospects. Systematic events can be looked at as disruptions to the market and cause a downward shift in stock prices.

Unsystematic Risk

Unsystematic risk includes company or industry specific events. For example, companies that produced radios were at risk when TVs became popular, companies that grow and sell vegetables are affected when there are weather events such as droughts or hurricanes that destroy their crops. These risks can greatly affect a stock and often cause sharp declines in prices.

Bond Price Movements

While stocks, or equity, are one way for a company to raise money, debt is another. Debt for a company is often raised in the form of bonds. Bonds are issued by large corporations such as Apple or Amazon, by cities such as New York or Los Angeles, by states such as Illinois or Florida and by countries like America, or Brazil. Bonds are issued by the entity and bought by the investor. Over time the entity will pay back an interest rate known as the coupon in addition to the principal. All bonds are issued at a par rate. This is the price of the bond when it is issued.

How Bonds Work

For example, let’s say Apple needs $100M to build a factory and decide to issue bonds with a maturity date in 10 years. Apple would identify an interest rate at which investors are confident with lending money. If the interest rate is 5%, Apple would need to give the investors 5% of the borrowed amount every year until the maturity date of the bond, the year the money will be returned. Bonds are usually issued in denominations of $1000.

Therefore, if you bought a $1000 bond from Apple, you would pay them the money today and receive 5% of 1000 ($50) every year for the next 10 years. At maturity, they pay back the $1000.

Interest Rates and Bonds

Bond prices, much like stock prices, experience fluctuations. The first and major implication is interest rate risk. Suppose you invest in a corporate bond that pays a fixed interest of 5% until maturity while the central bank interest rate is 2%. If the central bank rates rise while you own the bond to 4%, the price of your bond will fall.

This is because investors are always comparing the risk and return of your bond with anything else they could be investing in. If your bond pays 5% compared to the central rate of 2%, you are earning a 3% premium. If your premium drops to 1%, fewer other investors would be interested. Interest rates have an inverse relationship with bonds, as rates rise bond prices fall and vice versa.

Inflation and Bonds

A second factor in bond price fluctuation is inflation. Inflation is when the value of currency decreases over time. If a bond is paying a coupon rate of 5% on a $1000 bond, over 10 years the value of the coupon is worth less in the 10th year then the current one. As a result, the effective yield is lower as the market price of the bond decreases. As a result, we have a second inverse relationship, as inflation increases bond prices decrease, and vice versa.

Credit Ratings

Lastly credit ratings affect the price of bonds and cause fluctuation in prices. Credit Rating Agencies such as S&P Global Ratings, Moody’s, and Fitch conduct investment analysis on companies and assign independent debt ratings. Ratings go from AAA, which indicate a very low probability of failing to make bond payments to investors, to D a complete default of the debt. When the debt rating for a company goes up, the price of the bonds increase accordingly, and any new bonds they release will have a lower interest rate. A downgrade is followed by bond prices falling, and any new bonds issued coming with a much higher interest rate. This lesson is part of the PersonalFinanceLab curriculum library. Schools with a PersonalFinanceLab.com site license can get this lesson, plus our full library of 300 others, along with our budgeting game, stock game, and automatically-graded assessments for their classroom - complete with LMS integration and rostering support!

Get PersonalFinanceLab

[qsm quiz=141]

In the old west, a brand served as a symbol which quickly communicated a message of who owned that brand. Today, a brand performs the same function and much more. A company’s brand communicates the company’s image or how the business wants to present itself to and be perceived by the public.

In the old west, a brand served as a symbol which quickly communicated a message of who owned that brand. Today, a brand performs the same function and much more. A company’s brand communicates the company’s image or how the business wants to present itself to and be perceived by the public. Another ethical and legal issue in planning business advertising is copyright infringement. This occurs when a business purposefully or inadvertently uses legally protected images, trademarks, or other material in advertising without the permission or remuneration of the protected material. Using a photograph taken from the internet for an ad may represent the image you want, but the photographer who took the shot and owns its copyright will probably sue you.

Another ethical and legal issue in planning business advertising is copyright infringement. This occurs when a business purposefully or inadvertently uses legally protected images, trademarks, or other material in advertising without the permission or remuneration of the protected material. Using a photograph taken from the internet for an ad may represent the image you want, but the photographer who took the shot and owns its copyright will probably sue you. Broadcast advertising includes, AM and FM radio as well as broadcast and cable television. Each of these media methods appeal to varying audiences and therefore their use must be part of a comprehensive business advertising plan. For example, AM radio stations hold a different demographic of listeners than FM radio stations. Cable news networks possess different audiences than cable movie channels, and broadcast stations seek a variety of viewers.

Broadcast advertising includes, AM and FM radio as well as broadcast and cable television. Each of these media methods appeal to varying audiences and therefore their use must be part of a comprehensive business advertising plan. For example, AM radio stations hold a different demographic of listeners than FM radio stations. Cable news networks possess different audiences than cable movie channels, and broadcast stations seek a variety of viewers.

This specific financial ratio has been very useful over the past year with regards to the slump in retail stores due to online shopping. Nordstrom has a P/S ratio of 0.530 and Macy’s has a P/S ratio of 0.280. This is a great tool for valuing an asset in comparison to another in terms of sales. This ratio shows that Nordstrom’s current market cap is much lower than it could be in terms of their revenue compared to Macy’s – per dollar value of the company, Macy’s is making more sales.

This specific financial ratio has been very useful over the past year with regards to the slump in retail stores due to online shopping. Nordstrom has a P/S ratio of 0.530 and Macy’s has a P/S ratio of 0.280. This is a great tool for valuing an asset in comparison to another in terms of sales. This ratio shows that Nordstrom’s current market cap is much lower than it could be in terms of their revenue compared to Macy’s – per dollar value of the company, Macy’s is making more sales.

When investing, an investor deposits money within an account with their broker. There is a choice of two types of accounts in which to deposit the money: a cash account or a margin account.

When investing, an investor deposits money within an account with their broker. There is a choice of two types of accounts in which to deposit the money: a cash account or a margin account.

Market timing is an investment strategy where the investor buys or shorts stocks and financial instruments based on their expectations of what might happen in the market. This is the “Buy low, sell high” idea – trying to buy stocks just before the prices go up, and selling them at the peak.

Market timing is an investment strategy where the investor buys or shorts stocks and financial instruments based on their expectations of what might happen in the market. This is the “Buy low, sell high” idea – trying to buy stocks just before the prices go up, and selling them at the peak. A portfolio has an international investment strategy if it has investments in foreign markets. An international investment strategy offers the investor the opportunity to lower the risk of their portfolio and to take advantage of possible investment opportunities in foreign markets. It reduces risk through diversifying. Diversifying is where the investor invests in more than one market to reduce the risk to any specific market. Instead of being fully invested in domestic markets, the domestic market holds a smaller percentage of investments with investments in foreign markets making up the rest of the portfolio. If the investor was to only focus on American markets and if the markets took a dive, it would be very difficult to protect the portfolio from taking a hit. Therefore, if they had investments in many markets internationally, the investments in other markets would be safe. The investor’s portfolio of investments would not be as exposed.

A portfolio has an international investment strategy if it has investments in foreign markets. An international investment strategy offers the investor the opportunity to lower the risk of their portfolio and to take advantage of possible investment opportunities in foreign markets. It reduces risk through diversifying. Diversifying is where the investor invests in more than one market to reduce the risk to any specific market. Instead of being fully invested in domestic markets, the domestic market holds a smaller percentage of investments with investments in foreign markets making up the rest of the portfolio. If the investor was to only focus on American markets and if the markets took a dive, it would be very difficult to protect the portfolio from taking a hit. Therefore, if they had investments in many markets internationally, the investments in other markets would be safe. The investor’s portfolio of investments would not be as exposed.

Upper managements such as the chief executive officers (CEO), the chief financial officer (CFO), the chief operating officer (COO), the chief technology officer (CTO), the chief marketing officer (CMO), the directors, the presidents, the senior vice presidents, the vice presidents, the sales managers, and many others are charged with being the role models, supporters, the enforcers, the implementers, and the delegators of social responsibility. In other words, social responsibility usually comes from the top, with the highest-level managers encouraging their subordinates to act with social responsibility. This is usually done through the company’s mission and vision statements, implementations of internal controls, and specific goals laid out in the business plan.

Upper managements such as the chief executive officers (CEO), the chief financial officer (CFO), the chief operating officer (COO), the chief technology officer (CTO), the chief marketing officer (CMO), the directors, the presidents, the senior vice presidents, the vice presidents, the sales managers, and many others are charged with being the role models, supporters, the enforcers, the implementers, and the delegators of social responsibility. In other words, social responsibility usually comes from the top, with the highest-level managers encouraging their subordinates to act with social responsibility. This is usually done through the company’s mission and vision statements, implementations of internal controls, and specific goals laid out in the business plan. Being and becoming socially responsible is about working with people who are able to identify when something is socially responsible or irresponsible. Social responsibility is about listening and learning about the people and the environment from which it will apply. Being constructive means listening to complaints, coming from both inside and outside of the organization, and being willing to act on those complaints.

Being and becoming socially responsible is about working with people who are able to identify when something is socially responsible or irresponsible. Social responsibility is about listening and learning about the people and the environment from which it will apply. Being constructive means listening to complaints, coming from both inside and outside of the organization, and being willing to act on those complaints. Companies get the best press if they are proactive and address social issues before they are forced to do so by government regulation. For example, the Heinz brand became nationally beloved after it became the first major

Companies get the best press if they are proactive and address social issues before they are forced to do so by government regulation. For example, the Heinz brand became nationally beloved after it became the first major  Inviting the public (current, future, and potential customers) to share their thoughts and ideas of how the company can improve their products and services and reaching out to the public to help solve problems. Whenever you take a survey or write a review, all that data is used by the company to make a change.

Inviting the public (current, future, and potential customers) to share their thoughts and ideas of how the company can improve their products and services and reaching out to the public to help solve problems. Whenever you take a survey or write a review, all that data is used by the company to make a change. The federal government had to respond to this one because people were getting tricked into buying things over the phone by people pretending to sell them something they needed. In return, people gave these fraudsters their personal and financial information. Investigators reported that each year there were $40 billion of losses because of these indirect phishing schemes and Congress responded. This act makes it illegal for telemarketers to deceive and coerce customers and requires them to disclose their information and only make calls at certain times of the day.

The federal government had to respond to this one because people were getting tricked into buying things over the phone by people pretending to sell them something they needed. In return, people gave these fraudsters their personal and financial information. Investigators reported that each year there were $40 billion of losses because of these indirect phishing schemes and Congress responded. This act makes it illegal for telemarketers to deceive and coerce customers and requires them to disclose their information and only make calls at certain times of the day.

Internal Controls are the procedures and processes in place at an organization to make sure everything operates smoothly and mistakes stay rare. This includes things like building Standard Operating Procedures (SOPs), Quality Assurance (QA), and Auditing. It also includes checks and investigations to make sure those SOPs and QA processes are being followed properly, not just unused documents. Most of the examples in this article will focus on internal risk management.

Internal Controls are the procedures and processes in place at an organization to make sure everything operates smoothly and mistakes stay rare. This includes things like building Standard Operating Procedures (SOPs), Quality Assurance (QA), and Auditing. It also includes checks and investigations to make sure those SOPs and QA processes are being followed properly, not just unused documents. Most of the examples in this article will focus on internal risk management. Internal Risk Control is what a manager and organization put in place to minimize risks coming from inside the organization. These controls fall into 4 broad categories:

Internal Risk Control is what a manager and organization put in place to minimize risks coming from inside the organization. These controls fall into 4 broad categories: Before a risk can be assessed, the first step is identifying what exactly that risk is. The goal of Step 1 is to have a clear and concise definition of what exactly the potential problems are and what kinds of damage might be caused. For example, dangerous machines in a workplace have a defined risk of harming workers, which both loses productivity and results in lawsuits.

Before a risk can be assessed, the first step is identifying what exactly that risk is. The goal of Step 1 is to have a clear and concise definition of what exactly the potential problems are and what kinds of damage might be caused. For example, dangerous machines in a workplace have a defined risk of harming workers, which both loses productivity and results in lawsuits. Effective controls are implemented on a trial basis. This means the team has a training session to outline what the hazards are and the new controls being implemented to address them. While the trial progresses, the entire team (from rank-and-file workers through the management involved) record how the implementation impacts their work, both in terms of actually addressing the risks the controls are addressing and the realized cost of implementing them.

Effective controls are implemented on a trial basis. This means the team has a training session to outline what the hazards are and the new controls being implemented to address them. While the trial progresses, the entire team (from rank-and-file workers through the management involved) record how the implementation impacts their work, both in terms of actually addressing the risks the controls are addressing and the realized cost of implementing them. Audits are larger reviews of the internal risk controls that a company has implemented. Audits are separate from the normal risk assessment procedures, but do follow a similar road map for how they are conducted.

Audits are larger reviews of the internal risk controls that a company has implemented. Audits are separate from the normal risk assessment procedures, but do follow a similar road map for how they are conducted.

The Series 6 exam (Investment Company and Variable Contracts Products Representative Exam) consists of 100 multiple choice questions, takes 2 hours and 15 minutes to complete, and costs $100. The passing score is 70%. A candidate who passes this exam is able to solicit, buy, and/or sell mutual funds and variable annuities.

The Series 6 exam (Investment Company and Variable Contracts Products Representative Exam) consists of 100 multiple choice questions, takes 2 hours and 15 minutes to complete, and costs $100. The passing score is 70%. A candidate who passes this exam is able to solicit, buy, and/or sell mutual funds and variable annuities. A Certified Financial Planner is administered by the

A Certified Financial Planner is administered by the

Planning is a combination of analysis and outlining a plan of action. Planning is what you want to do to achieve some goal or objective to help better manage a business. The purpose of planning is to plan what direction the business is headed, what decisions need to be made, how to be better than competitors in the same industry and business, and how to eliminate wastefulness and optimize current operations. Since plans address a huge variety of business objectives, they tend to be very diverse themselves, but all good plans have a few core components:

Planning is a combination of analysis and outlining a plan of action. Planning is what you want to do to achieve some goal or objective to help better manage a business. The purpose of planning is to plan what direction the business is headed, what decisions need to be made, how to be better than competitors in the same industry and business, and how to eliminate wastefulness and optimize current operations. Since plans address a huge variety of business objectives, they tend to be very diverse themselves, but all good plans have a few core components: A “Business Plan” in this context is the core document of a small business – it merges many elements of both Strategic Planning and Business Planning together to present one clear vision of what a company is, what its goals are, and how it seeks to achieve them. A good business plan serves three functions: it provides direction to all levels of management as to where the company is heading (like a Strategic Plan), it provides guidance for what a company’s goals and missions are to the rank-and-file workers at a business, and it serves as a document to present to banks and other investors to show why a company will be profitable.

A “Business Plan” in this context is the core document of a small business – it merges many elements of both Strategic Planning and Business Planning together to present one clear vision of what a company is, what its goals are, and how it seeks to achieve them. A good business plan serves three functions: it provides direction to all levels of management as to where the company is heading (like a Strategic Plan), it provides guidance for what a company’s goals and missions are to the rank-and-file workers at a business, and it serves as a document to present to banks and other investors to show why a company will be profitable. Reveals the possible strengths, weaknesses, opportunities, and threats that your company will encounter in internal and external business environment.

Reveals the possible strengths, weaknesses, opportunities, and threats that your company will encounter in internal and external business environment. Planning and locating the procurement, distribution, and exchange of supplies and materials to reduce shipping time and decrease shipping costs.

Planning and locating the procurement, distribution, and exchange of supplies and materials to reduce shipping time and decrease shipping costs. Crowdsourced plans farm out most of the “heavy lifting” to a large number of people. Companies with strong cohesion of their low-level managers and workers can find great success when crowdsourcing business plans, because it gives all of the people involved a greater “stake” in helping define what company goals are attainable.

Crowdsourced plans farm out most of the “heavy lifting” to a large number of people. Companies with strong cohesion of their low-level managers and workers can find great success when crowdsourcing business plans, because it gives all of the people involved a greater “stake” in helping define what company goals are attainable. For instance, when it comes to organizing in the logistics department, the manager plans the structure of when shipments will be made, at what times, how long the shipments should be, at what facilities they should be distributed to reduce shipping costs. The manager also needs to plan how much supplies will be allocated to each factory, how much each factory will produce, how much of that product will be shipped to facilities, and where should they be distributed. The manager leads in the structure and allocation of what happens in the logistics department by planning how to get workers to do what is asked and expected of them so that the work process and item production are operating at the highest level. However, when problems arise the manager must control the situation by planning how to solve the problem and how to prevent it from happening again. Planning is in everywhere and everything the manager does.

For instance, when it comes to organizing in the logistics department, the manager plans the structure of when shipments will be made, at what times, how long the shipments should be, at what facilities they should be distributed to reduce shipping costs. The manager also needs to plan how much supplies will be allocated to each factory, how much each factory will produce, how much of that product will be shipped to facilities, and where should they be distributed. The manager leads in the structure and allocation of what happens in the logistics department by planning how to get workers to do what is asked and expected of them so that the work process and item production are operating at the highest level. However, when problems arise the manager must control the situation by planning how to solve the problem and how to prevent it from happening again. Planning is in everywhere and everything the manager does.

Here, sellers gather as much relevant information as possible prior to the appointment with the customer. This focuses on new customers where information is collected in such a way that it has enough applicability and usefulness for effective use. This can be looking up a customer on their social media accounts and finding their likes, dislikes, and needs to present this information in relation to the product.

Here, sellers gather as much relevant information as possible prior to the appointment with the customer. This focuses on new customers where information is collected in such a way that it has enough applicability and usefulness for effective use. This can be looking up a customer on their social media accounts and finding their likes, dislikes, and needs to present this information in relation to the product. The last part of the presentation and the most fearful for the seller. But have no fear! Closing the sale is only confirming and understanding, the fear will disappear if the seller TRULY believes that the customer will enjoy the benefits after they made the purchase.

The last part of the presentation and the most fearful for the seller. But have no fear! Closing the sale is only confirming and understanding, the fear will disappear if the seller TRULY believes that the customer will enjoy the benefits after they made the purchase. Improvements in technology are drastically changing the communication between buyers and sellers. This phenomenon is referred to as a revolution in sales. Technology is an amazing factor in the personal selling process, and allows for products and services to be sold in a variety of different ways. Social Media and the Internet contributed a great deal to this revolution. Customers still want relationships, but look for it in different ways. With more and more people buying online, relationships and repeating customers have to be brought in – in a completely different way. Sellers are no longer meeting face to face with each customer, and need another way to build trust. You might have already seen one way companies address this – many websites have an online chat feature that allows a potential customer to communicate with a seller and then partake in the 8-step process above.

Improvements in technology are drastically changing the communication between buyers and sellers. This phenomenon is referred to as a revolution in sales. Technology is an amazing factor in the personal selling process, and allows for products and services to be sold in a variety of different ways. Social Media and the Internet contributed a great deal to this revolution. Customers still want relationships, but look for it in different ways. With more and more people buying online, relationships and repeating customers have to be brought in – in a completely different way. Sellers are no longer meeting face to face with each customer, and need another way to build trust. You might have already seen one way companies address this – many websites have an online chat feature that allows a potential customer to communicate with a seller and then partake in the 8-step process above. Be careful of the small talk, some cultures believe that it makes someone appear untrustworthy. In America, although tedious to some, small talk is normal. However, in some other cultures, talking about personal life before talking about a business deal can cause the customer to feel uneasy about the seller and may view them as mischievous.

Be careful of the small talk, some cultures believe that it makes someone appear untrustworthy. In America, although tedious to some, small talk is normal. However, in some other cultures, talking about personal life before talking about a business deal can cause the customer to feel uneasy about the seller and may view them as mischievous.

Executive role – The HR department are specialists in areas that encompass the management of employees.

Executive role – The HR department are specialists in areas that encompass the management of employees. Choosing and hiring employees – The HR department oversees setting job qualifications and sifting through résumés and choosing the most qualified candidate for the interview.

Choosing and hiring employees – The HR department oversees setting job qualifications and sifting through résumés and choosing the most qualified candidate for the interview.

What is and is not “Ethical” is often very subjective. Over time, several different ways of defining ethical behavior have arisen.

What is and is not “Ethical” is often very subjective. Over time, several different ways of defining ethical behavior have arisen. All businesses are based on a foundation of trust. Customers expect to get their money’s worth from a product they buy (that it will do what is advertised, is free from defect, and is safe to use). Investors expect to know how their money is being used to run the business (though accurate financial statements, truthful statements from the management, and adherence to core principles). Nothing destroys a business faster than losing the public trust, which is why maintaining strong business ethics is essential in the business world today.

All businesses are based on a foundation of trust. Customers expect to get their money’s worth from a product they buy (that it will do what is advertised, is free from defect, and is safe to use). Investors expect to know how their money is being used to run the business (though accurate financial statements, truthful statements from the management, and adherence to core principles). Nothing destroys a business faster than losing the public trust, which is why maintaining strong business ethics is essential in the business world today. The government actively monitors companies throughout the country, through quality control tests on products, audits of tax forms and financial statements, and other avenues. If unethical behavior is discovered by the government, a company will usually face extremely stiff penalties, and the management may be criminally liable. The company will also likely be forced to engage in lengthy and expensive legal battles, and may have its reputation irreparably damaged.

The government actively monitors companies throughout the country, through quality control tests on products, audits of tax forms and financial statements, and other avenues. If unethical behavior is discovered by the government, a company will usually face extremely stiff penalties, and the management may be criminally liable. The company will also likely be forced to engage in lengthy and expensive legal battles, and may have its reputation irreparably damaged. You probably will not see a business’s Code of Ethics until after you start. For most employees, they usually do not even take a good look until a major ethical issue has already come up, but your life will be made much easier by evaluating the Code of Ethics early, and bringing up any concerns with your managers before issues arise.

You probably will not see a business’s Code of Ethics until after you start. For most employees, they usually do not even take a good look until a major ethical issue has already come up, but your life will be made much easier by evaluating the Code of Ethics early, and bringing up any concerns with your managers before issues arise. This act was created in the wake of the Enron Collapse. Enron was a company that primarily dealt with energy. Throughout the late 2000’s, the corporate culture of Enron was obsessed with driving Growth At Any Cost – the company’s daily stock price was posted in the elevators, and associate bonuses were based almost entirely on short-term gains. At lower levels of management, managers were found to have been artificially manipulating energy levels in several states, causing artificial shortages to drive up energy prices. At higher levels, senior managers were found to be manipulating the “book value” of many assets to make failing assets seem profitable. Eventually the entire company collapsed when journalists began investigating their seemingly impossible winning streak, bringing down both one of the biggest energy companies in the world, and one of the most (formally) trusted accounting firms.

This act was created in the wake of the Enron Collapse. Enron was a company that primarily dealt with energy. Throughout the late 2000’s, the corporate culture of Enron was obsessed with driving Growth At Any Cost – the company’s daily stock price was posted in the elevators, and associate bonuses were based almost entirely on short-term gains. At lower levels of management, managers were found to have been artificially manipulating energy levels in several states, causing artificial shortages to drive up energy prices. At higher levels, senior managers were found to be manipulating the “book value” of many assets to make failing assets seem profitable. Eventually the entire company collapsed when journalists began investigating their seemingly impossible winning streak, bringing down both one of the biggest energy companies in the world, and one of the most (formally) trusted accounting firms. Ahead of the Great Recession, many banks were issuing record numbers of sub-prime loans, or loans issued to lenders with poor credit history or low earnings. Sub-prime loans in and of themselves are not bad – they can be an important way to help uplift people from poverty. What was new was the introduction of wide-spread derivatives trading involving investment banks using something called derivatives and interest-rate swaps, which created a potential for abuse.

Ahead of the Great Recession, many banks were issuing record numbers of sub-prime loans, or loans issued to lenders with poor credit history or low earnings. Sub-prime loans in and of themselves are not bad – they can be an important way to help uplift people from poverty. What was new was the introduction of wide-spread derivatives trading involving investment banks using something called derivatives and interest-rate swaps, which created a potential for abuse.

When you are applying for a job, you should be triple-checking everything you want to send to your potential employer. Every job posting gets over

When you are applying for a job, you should be triple-checking everything you want to send to your potential employer. Every job posting gets over

This pitfall is the opposite of the previous – you are so concerned with getting an interview that you tried to cast a very wide net and make sure you always have applications sent out. This is a common problem because it is also a productive habit. Maybe you set a goal for yourself to find and apply for one new job every day, or spend 8 hours searching for a job every week.

This pitfall is the opposite of the previous – you are so concerned with getting an interview that you tried to cast a very wide net and make sure you always have applications sent out. This is a common problem because it is also a productive habit. Maybe you set a goal for yourself to find and apply for one new job every day, or spend 8 hours searching for a job every week. As we said in the intro, the job search process will last around 43 days for experienced workers, longer for fresh graduates. This application time is going to be stressful – probably a lot more stressful than any job you secure, so you should count your job search time as work.

As we said in the intro, the job search process will last around 43 days for experienced workers, longer for fresh graduates. This application time is going to be stressful – probably a lot more stressful than any job you secure, so you should count your job search time as work.

Every year, the National Association of Colleges and Employers surveys internship participants about their experiences. For students who undertook paid internships, all the common knowledge of internships applied: students graduated with job offers nearly twice the rate of students with no internships (

Every year, the National Association of Colleges and Employers surveys internship participants about their experiences. For students who undertook paid internships, all the common knowledge of internships applied: students graduated with job offers nearly twice the rate of students with no internships (

Lower starting wages, barely better chances of getting a job, less interesting work while on the internship, why would students offer to work for free at all?

Lower starting wages, barely better chances of getting a job, less interesting work while on the internship, why would students offer to work for free at all? When you apply for an internship, all of the standard rules for job seekers apply.

When you apply for an internship, all of the standard rules for job seekers apply.

Try to look at the interview process from the perspective of the hiring manager. Like we have said before,

Try to look at the interview process from the perspective of the hiring manager. Like we have said before,  When you are interviewing for a job, the interviewer’s primary concern is whether or not you can do that job. If they get the impression that there is something you cannot, or will not, do, chances are they will move on to another candidate. This does not mean you should overstate your qualifications or say you can do something you can’t. Instead, if there is a part of the position you feel under-qualified to fill, mention that you would need some extra training for that aspect.

When you are interviewing for a job, the interviewer’s primary concern is whether or not you can do that job. If they get the impression that there is something you cannot, or will not, do, chances are they will move on to another candidate. This does not mean you should overstate your qualifications or say you can do something you can’t. Instead, if there is a part of the position you feel under-qualified to fill, mention that you would need some extra training for that aspect. The questions you ask are something unique to you, meaning this is where the interviewer leaves their prepared script. Asking questions makes the interviewer stop and think of a response, meaning it is one more hook that will help you stick in their mind later –

The questions you ask are something unique to you, meaning this is where the interviewer leaves their prepared script. Asking questions makes the interviewer stop and think of a response, meaning it is one more hook that will help you stick in their mind later – Just as you are reading this for tips on how to make a great impression during your interview, your interviewer is probably reading up on ways to filter candidates by asking the right questions on their end. This gives you an advantage, since you can easily look up common interview questions, and even

Just as you are reading this for tips on how to make a great impression during your interview, your interviewer is probably reading up on ways to filter candidates by asking the right questions on their end. This gives you an advantage, since you can easily look up common interview questions, and even

When you apply for a job, you already know you are not the only one. In fact, on average, companies receive

When you apply for a job, you already know you are not the only one. In fact, on average, companies receive  Big companies looking to fill a position need to be able to sift through hundreds of applications for every job. Since they are typically listing dozens of jobs at any given time, that means they need to be able to sort through thousands of resumes every day. Even extremely dedicated HR managers who have every intention to give every applicant a fair shot would not be able to handle the sheer volume of resumes and cover letters coming across his or her desk.

Big companies looking to fill a position need to be able to sift through hundreds of applications for every job. Since they are typically listing dozens of jobs at any given time, that means they need to be able to sort through thousands of resumes every day. Even extremely dedicated HR managers who have every intention to give every applicant a fair shot would not be able to handle the sheer volume of resumes and cover letters coming across his or her desk. Even if you get past the ATS, a study from TheLadders.com recently found that recruiters only spend about

Even if you get past the ATS, a study from TheLadders.com recently found that recruiters only spend about  The “High Value” keywords are the core job requirements that the hiring manager is almost certainly going to filter for. In this case, the recruiter outlined several:

The “High Value” keywords are the core job requirements that the hiring manager is almost certainly going to filter for. In this case, the recruiter outlined several: The “Low Hanging Fruit” keywords are the ones that the recruiter specifically outlines in the job posting, but they are less likely to be specifically searching for. These keywords come in to play during your Six Seconds the first hiring manager is filtering your resume. If you have some of the buzz words they have in mind for their ideal candidate, you are more likely to get a call back.

The “Low Hanging Fruit” keywords are the ones that the recruiter specifically outlines in the job posting, but they are less likely to be specifically searching for. These keywords come in to play during your Six Seconds the first hiring manager is filtering your resume. If you have some of the buzz words they have in mind for their ideal candidate, you are more likely to get a call back. A common pitfall of recent graduates starting their job search is a habit of adding in “puff pieces” or resume padding – these are words or phrases that make your resume look “fuller”, but do not add any relevant information for the recruiter. This tends to be an unfortunate side effect of padding to reach word limits on term papers and other academic writing projects, but it has no place in your job application.

A common pitfall of recent graduates starting their job search is a habit of adding in “puff pieces” or resume padding – these are words or phrases that make your resume look “fuller”, but do not add any relevant information for the recruiter. This tends to be an unfortunate side effect of padding to reach word limits on term papers and other academic writing projects, but it has no place in your job application.

Dog Bites. If you have a dog that bites someone, your premiums will immediately increase. This is the single most common reason why homeowners file insurance claims – their dog bites someone, who then sues for damages.

Dog Bites. If you have a dog that bites someone, your premiums will immediately increase. This is the single most common reason why homeowners file insurance claims – their dog bites someone, who then sues for damages.

Because convenience goods carry a relatively low price, consumers usually don’t bother price-checking—they simply stick with the brand they have always bought. For that reason, pricing isn’t overly important as long as the company doesn’t raise prices to the point of being significantly different from competitors. If someone always purchased Crest toothpaste for their entire life, they will not bother checking Colgate’s price to see if they can save a few cents; it’s a habitual purchase. Wide-scale promotion is very important in order to build brand recognition. Typically for a quick, impulsive purchase consumers will choose a brand that they have heard of and are familiar with (Heinz ketchup, for example, holds over 60% market share in the US largely because of its iconic brand). Strategic placement is also frequently used in an attempt to sell convenience goods. A common example is when stores will place candy and other small items right next to the checkout line in hopes of stirring up impulse purchases.

Because convenience goods carry a relatively low price, consumers usually don’t bother price-checking—they simply stick with the brand they have always bought. For that reason, pricing isn’t overly important as long as the company doesn’t raise prices to the point of being significantly different from competitors. If someone always purchased Crest toothpaste for their entire life, they will not bother checking Colgate’s price to see if they can save a few cents; it’s a habitual purchase. Wide-scale promotion is very important in order to build brand recognition. Typically for a quick, impulsive purchase consumers will choose a brand that they have heard of and are familiar with (Heinz ketchup, for example, holds over 60% market share in the US largely because of its iconic brand). Strategic placement is also frequently used in an attempt to sell convenience goods. A common example is when stores will place candy and other small items right next to the checkout line in hopes of stirring up impulse purchases. Strategically, product quality and pricing are much more important for shopping goods than for convenience goods. With customers actively weighing their options, it is vital for a company to provide an offering with attractive value. This can mean selling a product that is better quality than competitors for the same price or selling a product that is similar in quality but at a lower price. The larger the purchase, the more important marketing the good becomes because customers will more actively consider the product’s price-value relationship. Promotion is also important for shopping goods in order to differentiate a product from its competitors and to communicate the value proposition to customers. Whereas promoting convenience goods simply focused on awareness, promoting shopping goods must focus on separating a product from its competition in the minds of customers.

Strategically, product quality and pricing are much more important for shopping goods than for convenience goods. With customers actively weighing their options, it is vital for a company to provide an offering with attractive value. This can mean selling a product that is better quality than competitors for the same price or selling a product that is similar in quality but at a lower price. The larger the purchase, the more important marketing the good becomes because customers will more actively consider the product’s price-value relationship. Promotion is also important for shopping goods in order to differentiate a product from its competitors and to communicate the value proposition to customers. Whereas promoting convenience goods simply focused on awareness, promoting shopping goods must focus on separating a product from its competition in the minds of customers. Typically, consumers of specialty goods do not have much price sensitivity—they are willing to pay whatever price is necessary for the product or brand that they prefer. Someone purchasing a Ferrari likely doesn’t care if a similar car is a few thousand dollars cheaper; they are paying for the brand name and the social status that comes with owning a Ferrari. Therefore, more of the company’s strategic focus needs to be centered on developing outstanding and innovational products that will retain the loyalty of their following. Promotion focuses on demonstrating the company’s latest great product and when/where people can buy it. It is also important to promote status that comes with the brand.

Typically, consumers of specialty goods do not have much price sensitivity—they are willing to pay whatever price is necessary for the product or brand that they prefer. Someone purchasing a Ferrari likely doesn’t care if a similar car is a few thousand dollars cheaper; they are paying for the brand name and the social status that comes with owning a Ferrari. Therefore, more of the company’s strategic focus needs to be centered on developing outstanding and innovational products that will retain the loyalty of their following. Promotion focuses on demonstrating the company’s latest great product and when/where people can buy it. It is also important to promote status that comes with the brand. The key to marketing unsought goods is to remind consumers that the product exists and to convince them that they need to purchase the product to avoid future hardships. For example, a company might run an emotional campaign focusing on how the potential customer’s loved ones will suffer financially if the customer dies unexpectedly. If successful, this would convince the buyer that purchasing a policy is a payment toward protecting their family and they would be compelled to go through with it in order to not have to worry about the potential danger. A lot of promotion is necessary, because consumers rarely think about buying such products unless they are prompted to.

The key to marketing unsought goods is to remind consumers that the product exists and to convince them that they need to purchase the product to avoid future hardships. For example, a company might run an emotional campaign focusing on how the potential customer’s loved ones will suffer financially if the customer dies unexpectedly. If successful, this would convince the buyer that purchasing a policy is a payment toward protecting their family and they would be compelled to go through with it in order to not have to worry about the potential danger. A lot of promotion is necessary, because consumers rarely think about buying such products unless they are prompted to. There are certain issues or uncertainties within the product classification model that need to be taken into consideration. One problem is that certain goods can potentially fall under multiple categories. For example, certain customers may see diamonds as a shopping good and compare prices extensively between brands before making a purchase. Other consumers may have chosen one brand as the best (ie Tiffany & Co.) and they buy that brand for the quality and status it brings. Sometimes product classification can vary depending on the individual customer that is buying the good.

There are certain issues or uncertainties within the product classification model that need to be taken into consideration. One problem is that certain goods can potentially fall under multiple categories. For example, certain customers may see diamonds as a shopping good and compare prices extensively between brands before making a purchase. Other consumers may have chosen one brand as the best (ie Tiffany & Co.) and they buy that brand for the quality and status it brings. Sometimes product classification can vary depending on the individual customer that is buying the good.

There are two ways to reduce your tax bill – a “Deduction” and a “Tax Credit”.

There are two ways to reduce your tax bill – a “Deduction” and a “Tax Credit”. To make it easier to file taxes, everyone has the option to choose between “Itemized Deductions” or “Standard Deduction”. If you file an “Itemized Deduction”, you need to provide evidence of each item you’re deducting (like receipts and proof it is eligible), which can be very time consuming for small deductions.

To make it easier to file taxes, everyone has the option to choose between “Itemized Deductions” or “Standard Deduction”. If you file an “Itemized Deduction”, you need to provide evidence of each item you’re deducting (like receipts and proof it is eligible), which can be very time consuming for small deductions.

The Federal Child Tax Credit gives a simple tax credit for $1000 per child, up to a certain income threshold (between $55,000 and $110,000, depending on your marital status). If you earn more than this threshold, you will have $50 less tax credit for every $1000 over the threshold (so a married couple earning $120,000 would have a $950 tax credit). This tax credit is non-refundable.

The Federal Child Tax Credit gives a simple tax credit for $1000 per child, up to a certain income threshold (between $55,000 and $110,000, depending on your marital status). If you earn more than this threshold, you will have $50 less tax credit for every $1000 over the threshold (so a married couple earning $120,000 would have a $950 tax credit). This tax credit is non-refundable.  While you cannot write off any costs incurred in a job search, if you need to move between cities when you get a job, you can usually write off part of the moving expense. This is a deduction, subtracted from your taxable income.

While you cannot write off any costs incurred in a job search, if you need to move between cities when you get a job, you can usually write off part of the moving expense. This is a deduction, subtracted from your taxable income.  If you have a mortgage, some or all of your interest will be tax-deductible. Not all mortgage interest is tax-deductible – you need to provide evidence that your mortgage was taken out to buy your primary residence, or used for extensive renovations, and only applies to interest paid on loans up to $1 million. If your mortgage does not qualify, you can still write off the interest on the first $100,000 of your loan.

If you have a mortgage, some or all of your interest will be tax-deductible. Not all mortgage interest is tax-deductible – you need to provide evidence that your mortgage was taken out to buy your primary residence, or used for extensive renovations, and only applies to interest paid on loans up to $1 million. If your mortgage does not qualify, you can still write off the interest on the first $100,000 of your loan.  The “Saver’s Credit” is another word for the Retirement Savings Contribution Credit – the purpose of this credit is to encourage saving in retirement accounts and IRAs. This credit is for up to $2000, and is calculated as a percentage of your contributions (either 50%, 20%, or 10%, depending on your income).

The “Saver’s Credit” is another word for the Retirement Savings Contribution Credit – the purpose of this credit is to encourage saving in retirement accounts and IRAs. This credit is for up to $2000, and is calculated as a percentage of your contributions (either 50%, 20%, or 10%, depending on your income).

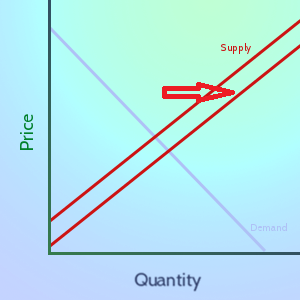

Supply and demand are among the most basic factors on market price for goods, and often an individual firm has little control over them. When there is an oversupply of a product in the market, assuming constant demand, the price of the good will decrease as firms attempt to unload their excess of inventory. Companies that refuse to lower price during a period of oversupply can be punished with huge drops in sales and a buildup of inventory they can’t get rid of. Oil is a prime example of an industry that is currently in oversupply—increased production has led to prices falling from well over $100/barrel down to around $50/barrel today.

Supply and demand are among the most basic factors on market price for goods, and often an individual firm has little control over them. When there is an oversupply of a product in the market, assuming constant demand, the price of the good will decrease as firms attempt to unload their excess of inventory. Companies that refuse to lower price during a period of oversupply can be punished with huge drops in sales and a buildup of inventory they can’t get rid of. Oil is a prime example of an industry that is currently in oversupply—increased production has led to prices falling from well over $100/barrel down to around $50/barrel today. Line pricing is when a company offers products at several different levels of quality (typically low, medium, and high). Pricing is set to reflect the relative quality of each offering, so the low-quality product would be at a discount price, the medium product would be at an average price, and the high-quality product would be at a premium price. The iPad is an example of this strategy—customers have the choice of buying a very basic model or they can pay several hundred dollars more to get one with higher quality and better features. As its name indicates, the line strategy is effective when a firm has a product line with several items that have a distinct difference in quality level. Segmented pricing can help clarify to consumers the added value that buying a better model entails and it provides customers some flexibility on deciding how much they want to spend.

Line pricing is when a company offers products at several different levels of quality (typically low, medium, and high). Pricing is set to reflect the relative quality of each offering, so the low-quality product would be at a discount price, the medium product would be at an average price, and the high-quality product would be at a premium price. The iPad is an example of this strategy—customers have the choice of buying a very basic model or they can pay several hundred dollars more to get one with higher quality and better features. As its name indicates, the line strategy is effective when a firm has a product line with several items that have a distinct difference in quality level. Segmented pricing can help clarify to consumers the added value that buying a better model entails and it provides customers some flexibility on deciding how much they want to spend. The loss leader strategy involves a company selling certain items at a loss in order to bring customers into the store. The assumption is that once customers are tempted into the store, they will have a tendency to buy other things as well that will generate the profit for the company. One very basic example of this are restaurants that sell kids’ meals for very cheap (even for free sometimes). The restaurant loses money on the kids’ meal, but makes their profit when the adults accompanying the children have to order full-price meals. This can be an effective strategy to generate store traffic, but firms must be careful to make sure that customers actually are buying products besides just the loss leaders.

The loss leader strategy involves a company selling certain items at a loss in order to bring customers into the store. The assumption is that once customers are tempted into the store, they will have a tendency to buy other things as well that will generate the profit for the company. One very basic example of this are restaurants that sell kids’ meals for very cheap (even for free sometimes). The restaurant loses money on the kids’ meal, but makes their profit when the adults accompanying the children have to order full-price meals. This can be an effective strategy to generate store traffic, but firms must be careful to make sure that customers actually are buying products besides just the loss leaders. Psychological pricing is an approach where prices are set based upon a psychological reaction that they will cause consumers. The ultimate goal of this tactic is to increase sales without significantly reducing prices. The most common example of this is when retailers price items one penny below an even dollar amount, $9.99 instead of $10 for example. Customers associate the $9.99 with the lower dollar amount of $9 rather than actively realizing that it is just one cent below $10. The massive usage of that tactic alone illustrates the success psychological pricing can have. It can be effective both for relatively low cost goods like gasoline or for big purchases like cars– $19,999.99 for some reason just seems a lot cheaper than $20,000.

Psychological pricing is an approach where prices are set based upon a psychological reaction that they will cause consumers. The ultimate goal of this tactic is to increase sales without significantly reducing prices. The most common example of this is when retailers price items one penny below an even dollar amount, $9.99 instead of $10 for example. Customers associate the $9.99 with the lower dollar amount of $9 rather than actively realizing that it is just one cent below $10. The massive usage of that tactic alone illustrates the success psychological pricing can have. It can be effective both for relatively low cost goods like gasoline or for big purchases like cars– $19,999.99 for some reason just seems a lot cheaper than $20,000. Technology has led to a very different environment for pricing than has been the norm in the past. With an increased ability to quickly “price-check” online, customers have become more sensitive to prices and it is more important to either be priced below competitors or to clearly communicate the brand’s superiority to consumers. It is also easier for customers to switch brands in that they can shop online and avoid having to travel to multiple stores to find the best deal. In these ways, additional power has shifted to the consumer in determining the way prices are set.

Technology has led to a very different environment for pricing than has been the norm in the past. With an increased ability to quickly “price-check” online, customers have become more sensitive to prices and it is more important to either be priced below competitors or to clearly communicate the brand’s superiority to consumers. It is also easier for customers to switch brands in that they can shop online and avoid having to travel to multiple stores to find the best deal. In these ways, additional power has shifted to the consumer in determining the way prices are set.

Revenue represents income earned by the firm through the primary goods and/or services provided. It is the income earned from the firm’s operating activities. For example, Mike’s Computers specializes in selling computers to small businesses. During the year, he sells 10,000 computers at $800, and nothing else. The total sales from the computers sold during the year, $8,000,000, would be Mike’s revenue.

Revenue represents income earned by the firm through the primary goods and/or services provided. It is the income earned from the firm’s operating activities. For example, Mike’s Computers specializes in selling computers to small businesses. During the year, he sells 10,000 computers at $800, and nothing else. The total sales from the computers sold during the year, $8,000,000, would be Mike’s revenue. Expenses can either be capitalized or expensed. Capitalization effectively means the cost of an assets can spread out over the life of an asset. A machine, for example, may be capitalized rather than expensed because the asset has a long useful life.

Expenses can either be capitalized or expensed. Capitalization effectively means the cost of an assets can spread out over the life of an asset. A machine, for example, may be capitalized rather than expensed because the asset has a long useful life. Losses are similar to gains in that both are recognized on the income statement only when an asset is sold and a loss is taken. Like gains, there can also be unrealized losses.

Losses are similar to gains in that both are recognized on the income statement only when an asset is sold and a loss is taken. Like gains, there can also be unrealized losses.

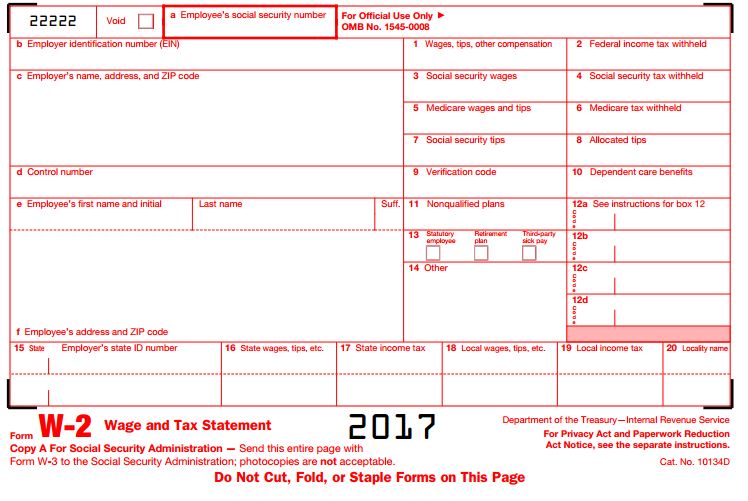

Income tax is the tax you pay on your income, usually directly taken out of your paycheck. Everyone who works in the United States should be paying income tax on their earnings.

Income tax is the tax you pay on your income, usually directly taken out of your paycheck. Everyone who works in the United States should be paying income tax on their earnings. The

The  The basic income tax return form in the United States is known as the

The basic income tax return form in the United States is known as the  The IRS may also apply corrections directly based on their own calculations of your taxes owed. If this is the case, they will generally mail you a letter explaining how their calculation differs from theirs, along with a method to dispute their calculation.

The IRS may also apply corrections directly based on their own calculations of your taxes owed. If this is the case, they will generally mail you a letter explaining how their calculation differs from theirs, along with a method to dispute their calculation.

The purpose of the Financial Accounting Standards Board (FASB) is to establish and improve US GAAP. There are also auditing standards, enforced by the Public Company Accounting Oversight Board (PCAOB), and required by the SEC. The purpose of the PCAOB is to protect the public interest in the preparation of audit reports. The FASB and PCAOB are responsible for the oversight of all United States accounting. Internationally, the IFRS Foundation and the International Accounting Standards Board (IASB) oversee international accounting.

The purpose of the Financial Accounting Standards Board (FASB) is to establish and improve US GAAP. There are also auditing standards, enforced by the Public Company Accounting Oversight Board (PCAOB), and required by the SEC. The purpose of the PCAOB is to protect the public interest in the preparation of audit reports. The FASB and PCAOB are responsible for the oversight of all United States accounting. Internationally, the IFRS Foundation and the International Accounting Standards Board (IASB) oversee international accounting. To remedy this, the Sarbanes-Oxley Act of 2002 (SOX) was passed by U.S. Congress in 2002. The SOX Act is a United States federal law that introduced major change to the regulation of financial disclosures and corporate governance. The SOX Act has closed loopholes in accounting practices and increased the consequences for fraudulent activity. The accounting profession is constantly changing and must adapt effectively and efficiently to meet the demands of the economy and society. Developments in the accounting profession, economy, and society affect the profession and how it performs its role. The SOX Act is one example of how a new regulation forced the profession to adapt to change.

To remedy this, the Sarbanes-Oxley Act of 2002 (SOX) was passed by U.S. Congress in 2002. The SOX Act is a United States federal law that introduced major change to the regulation of financial disclosures and corporate governance. The SOX Act has closed loopholes in accounting practices and increased the consequences for fraudulent activity. The accounting profession is constantly changing and must adapt effectively and efficiently to meet the demands of the economy and society. Developments in the accounting profession, economy, and society affect the profession and how it performs its role. The SOX Act is one example of how a new regulation forced the profession to adapt to change. Accountants regularly face ethical dilemmas. Accountants seek to add value by reducing costs and increasing revenue. An accountant wants to produce favorable results for their company or client. Accountants must also have the public best interest in mind. Therefore, information must be represented fairly and accurately to be ethical.

Accountants regularly face ethical dilemmas. Accountants seek to add value by reducing costs and increasing revenue. An accountant wants to produce favorable results for their company or client. Accountants must also have the public best interest in mind. Therefore, information must be represented fairly and accurately to be ethical.

The introduction stage marks the very first time a company brings a product to market. The main objective for companies at the beginning is not profit (often new products will generate losses because of high advertising costs and low sales) but rather developing a market for the product and building awareness among consumers. If successful, the company can then enjoy a better ROI in future stages as sales grow and relative costs lessen. An example of a product in the introduction stage could be when Amazon first rolled out their

The introduction stage marks the very first time a company brings a product to market. The main objective for companies at the beginning is not profit (often new products will generate losses because of high advertising costs and low sales) but rather developing a market for the product and building awareness among consumers. If successful, the company can then enjoy a better ROI in future stages as sales grow and relative costs lessen. An example of a product in the introduction stage could be when Amazon first rolled out their  If products make it through the introduction stage, they next advance to the growth period. This is when demand starts to take off for a product as companies promote to a wider audience in an attempt to build consumer preference over other brands and win market share. Because of increasing demand, companies are often able to start to make sizable profits in this stage. An example of a growth-stage product in today’s market could be drones; though they are a fairly new product, the market has been established and demand is rapidly growing.

If products make it through the introduction stage, they next advance to the growth period. This is when demand starts to take off for a product as companies promote to a wider audience in an attempt to build consumer preference over other brands and win market share. Because of increasing demand, companies are often able to start to make sizable profits in this stage. An example of a growth-stage product in today’s market could be drones; though they are a fairly new product, the market has been established and demand is rapidly growing. At some point, growth inevitably slows down and products reach the maturity stage. The top focus for managers at this point is protecting the market share they have earned, because the maturity stage is often the phase of the product life cycle with the most competition. Another key objective is to maximize profits—products in this phase of their life often turn into “cash cows” for companies that generate the funds necessary for developing new products. Apple’s (

At some point, growth inevitably slows down and products reach the maturity stage. The top focus for managers at this point is protecting the market share they have earned, because the maturity stage is often the phase of the product life cycle with the most competition. Another key objective is to maximize profits—products in this phase of their life often turn into “cash cows” for companies that generate the funds necessary for developing new products. Apple’s ( In the final stage of a product’s life, demand starts to decline as consumers move on to newer and more appealing products. Traditional telephones are an example of a product in this stage—with the emergence of cell phones, fewer and fewer people are using landlines and the market seems to be on its last legs.

In the final stage of a product’s life, demand starts to decline as consumers move on to newer and more appealing products. Traditional telephones are an example of a product in this stage—with the emergence of cell phones, fewer and fewer people are using landlines and the market seems to be on its last legs. While the product life cycle model is useful in many ways, it does have some issues. For one, there are products that do not seem to fit into the model. Brands like Coke (

While the product life cycle model is useful in many ways, it does have some issues. For one, there are products that do not seem to fit into the model. Brands like Coke (

What exactly is management? Is there only one way to manage? Management is the organization and coordination of the activities within a business to meet specific goals. Management creates policy and organizes, plans, controls, and directs a company’s resources to complete the objectives of that policy. Do all managers manage the same way? Do they all follow the same guidelines to meet their goals? As a matter of fact, management can be done in a number of different ways to achieve different goals within a business. The different ways managers define guidelines, set goals, and organize the company is collectively known as “Management Theories“, while the ideas behind ways managers interact with associates and lower-level managers are known as “Motivational Theories“. Some of the most prevalent management theories were first formulated by by Frederick Taylor, Max Weber and Henri Fayol, while some of the most potent motivational theories were formulated by Abraham Maslow, and Frederick Herzberg.