This research project accounts for 50% of the final mark. This will incorporate the use of StockTrak where you will ‘paper trade’ on a number of exchanges using a variety of derivatives and assets. You will set out targets for each trade, and interpret and evaluate the trading results in the context of the material read during the semester.

Students have 12 weeks to buy, sell, short, long and cover positions on trades made during this period.

Overview

Each trader has two accounts, each containing $1 million to trade. One account is known as the active account where you trade regularly, while the other account is known as the passive account.

To date the traders should use up all of the $1 million in the passive account on the purchase of stocks from a number of exchanges, as instructed. Traders will hold these stocks in their passive account for the duration of the trading period. Traders can adopt any approach in selecting these stocks.

The trades made in the Active account should reflect the material demonstrated and referred to in lectures, as well as those adopted by you having read outside the material, whether it is self-interest or adopted form from previous modules. Currently, the use of technical analysis will be discussed and, therefore, should be applied and reflected in the trades made.

Report Contents

The report should consist of:

• The traders’ strategy and level of risk (this could be a percentage of current funds, e.g. 5%. It is recommended that students do not trade a large percentage of their cash on individual trades).

• Reasons as to why the underlying has been traded (i.e. in the case of stocks, why it was purchased and/or short position taken). This may be speculative (given expected company reports, etc.) or a hedged position taken given other positions taken (in the case of options).

• The planned exit point for the trader. The trader should state before a trade is activated the point at which they will close out positions, e.g. in the case of futures, traders may state that they will close out a losing position once they lose X% or X amount of their trade on that derivative or asset. Also, they must highlight that they will close out on or before the expiration date.

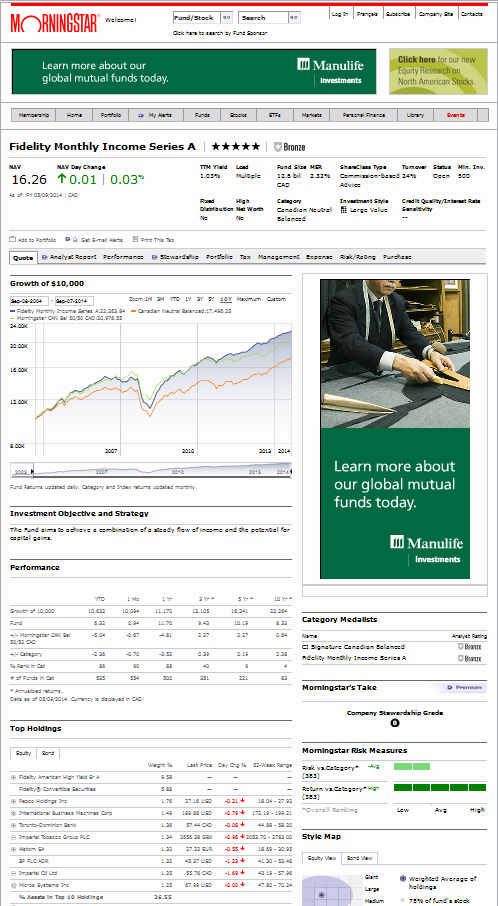

• If using fundamental or technical analysis to make speculative decisions on the future direction of the underlying, the trader must show the figures and/or graph in the report before the trade is activated highlighting their reasons. Once the trade has been reversed, the graph at the date of closing out the position should also be shown to highlight the movement in price. The trader must report the movement in price over the period on that trade and reflect on the traders’ own anticipation of the price movement.

• Traders must note that the prices shown for each underlying in each exchange reflects those in real markets and prices may be delayed by at least 15 minutes.

• It is recommended that traders be selective in their approach at the early stages of the report, i.e. get comfortable with the purchase of stocks in a few industries/exchanges. Also, traders should buy and short a few underlyings in the futures markets while using low volumes.

• It is very important to record the month you traded the derivative so that you can reverse the contract before maturity.

• Marks will be given for the variety of trades made that incorporates the material delivered in lectures, as well as those undertaken by the traders own initiative. Due to time restrictions, not all strategies can be addressed. Any student that is adventurous is more than welcome to use other strategies, which will be acknowledged by the examiner. The report is essential as it shows the traders’ activities and strategies. It is imperative that the report is started immediately. if the trader fails to wrote the report from the outset, it will cause problems later, therefore reflecting lack of quality and management of trades. This could possibly lead to losses, both in trades made and marks given for the assignment.

• Large profits may not be the deciding factor for marks awarded for this report (although they can be highly correlated with the traders astute awareness of price movements and proficient use of derivatives and strategies used). As long as the trader carries out trades and implements relevant strategies, and reports their entry and exit points, and reflects back on each outcome (whether it’s a losing or winning position), the report should merit a satisfactory grade.

There is no limit to the report, since trades activated by each trader can vary in number and/or discussion length. Enjoy the experience!

Lighten up the report by reporting on:

• How you were feeling at that particular time (tired, anxious, hungover, etc.)

• What you consumed prior to the trade (coffee) or the last time you had eaten.

You’d be surprised that some of the above could have resulted in loosing trades. If so, change your pattern and approach to making trades regarding the above and identify if trading outcomes change for the better or worse.

Any problems with Stocktrak, please note them in your report and email Stocktrak about them. These are considered your broker and trading platform.

Some Guidelines

“Fail to prepare, prepare to fail”

Stick to a couple of fundamental and /or technical analysis techniques for your trading, and ones that suit both your personality and psychology.

It is important to always follow the rules. Make up your own if you like, but always stick to the rules you adopt. And if the rules that you invent or adopt are bad ones, then change them.

As you gain experience in your trading life, it is the intensity of this experience that will be the greatest teacher.

Only use capital that you can afford to lose. Don’t bet your shirt. A rule of thumb is to never risk more than 5% of your trading capital on any one trade. For smaller accounts under €25,000, then 10% is fine.

Do not fall in love with a stock: doing so could have detrimental results on your profits.

Do not be greedy. Set a price target or exit strategy for your chosen stock, and if you reach this target, SELL or BUY (whichever is chosen outcome). If you do not, you could be falling in love with your stock!

Be disciplined. You will experience many highs and many lows, but hopefully the highs will outweigh the lows so that you won’t be wiped out.

There will be many challenges out there for you. Not only will you have to find what suits you but you must distinguish between the evangelical types who tell you how rich you’re going to become with their ‘amazing new techniques’, whilst you actually line their pockets, and the serious educators out there who are honest enough to tell you that it’s actually up to you.

Do not listen to the shoeshine boy or the taxi-driver. Markets may have reached its peak and it could be too late to get in. You’ll be burned.

It is possible to profit in a bear market and not just a bull. It is also possible to profit in a sideways market.

This has to become a hobby for you, one that you’ll enjoy and one that’s a continuing challenge.

The learning never stops. It’s incessant and compelling.

It’s best to avoid people promising you ludicrous returns per month and ‘guaranteed’ results with no effort on your part. If it looks too good to be true, it usually is!

You can make trading and investing an unusually predictable and successful vocation by your own efforts, enthusiasm and discipline.

Where possible, don’t fight the market. The market is more powerful than any one stock.

Have a trading buddy could help you to stick to your trading plan.

Get involved in physical activity so that the blood flows in a healthy way. Seek fresh air like walking the dog. It’ll free up the mind and will allow you to get away from work and strike some balance.

Keep a trade journal.

Criteria for successful trading:

Patience

Dream of all those luxury purchases that are the direct result of your successful trading. But don’t get excited and rush into it. Give yourself some time. Never start trading on an emotional wave of any kind. You need to be switched on, calm and alert. Give yourself time to learn.

Stick to your plan of action.

Patience also involves selecting a trading strategy where time works in your favour and where your downside is covered.

Be patient in your attitude in acquiring wealth. This doesn’t mean sitting back and doing nothing – that’s apathy and not patience.

Perseverance

If you believe in something, then you have to keep on it until you reach your goal. And once you’ve reached your goal, then set another target.

Having embarked on becoming a successful trader, you must stick to it. Babies do not give up trying to walk or talk after a few unsuccessful attempts. Follow their example and persevere and prepare yourself to be rewarded richly from this process of learning.

Give yourself attainable targets to reach in a realistic time frame. Get familiar with a few techniques at a time, especially the basic ones first.

Keep on setting attainable targets, making them slightly challenging, and this way your learning will gain momentum.

Your confidence will be built up.

Knowledge

Knowledge is attainable now with ease and speed. StockTrak will be used to simulate the trading experience and there are countless publications and web sites to help you build up your knowledge database.

Knowledge is experience. It is through extreme experiences that you find out a lot about yourself in good times and bad. If you encounter a terrible experience, step back, learn from your mistakes and apply what you’ve just learned. Don’t let trading success get to your head, as this is where you are at your most riskiest and dangerous (think of Nick Leeson!).

Honesty

Be honest with yourself if you want to be a decent trader – cut out the emotions of trading. You’re the one in control and the decision lies with you.

Don’t blame other people. Blaming the stock, the teacher or the tipster only wastes energy and stops you asking what more you can do to improve your technique, your knowledge and your performance.

Pre-Planning

You must pre-plan each and every trade. By doing this you must know your:

o maximum risk

o maximum reward

o breakeven points

You must also plan:

o your entry point

o your exit point whether it’s to:

take profit; or

stop losses

Discipline – the key to success

you must do your pre-planning every time

you use your (and others’) experience

you do not deviate from your stated sensible plan

By doing this you are becoming more mechanical and you are applying money management principles, thus ensuring that your losses are minimised and your profits are allowed to run.

To ask which one to choose is a very personal question that consists of a number of issues:

• What’s my own appetite for risk here?

• How does the stock behave?

• Where is the strongest support for the stock price?

• What are the charts telling me?

• What is the market telling me?

These questions will lead you to formulating a trading plan. In this particular case, there was strong support at the $20 level and that may impact on your eventual decision.

Keeping a Journal:

• Write down your stock picks and your reasons why every day.

• Write down the stock symbol, the direction in which you guess it’s heading, the reason for this (i.e. the Technical and Fundamental Analysis that is backing your judgement) and the appropriate time frame during which you anticipate the move to occur.

• When you make a trade, record the time of the trade, the strategy and any other relevant details that you think might affect your decision-making performance. Some highly successful traders take note of the weather, what they’ve eaten and drunk and all manner of other details, which they subsequently use to analyse their record and make adjustments to their Trading Plan.

“Cut your losses short and let your profits run”

If you’re wrong about the market, accept your losses before they snowball. The larger the loss, the more egg on your face. Do not wait in vain for the market to turn around and bail you out. Studies exist that indicate that staying too long with a losing position was one of the major reasons that speculators lost money. Willingness to close out a losing position early was identified as the mark of a successful (futures) trader.

Good Luck

The mere perception that a market is becoming Bearish is not a predictor of disaster. Fortunes have been made in

The mere perception that a market is becoming Bearish is not a predictor of disaster. Fortunes have been made in

Now that you know what an exchange is, it’s necessary to make a very important distinction between what shares trade on exchanges and what shares don’t.

Now that you know what an exchange is, it’s necessary to make a very important distinction between what shares trade on exchanges and what shares don’t.

Yet talk to any trader on the floor of an exchange and they’ll tell you it all works well. While it appears to be total, unbridled chaos, the system has worked for many years and continues to be effective today.

Yet talk to any trader on the floor of an exchange and they’ll tell you it all works well. While it appears to be total, unbridled chaos, the system has worked for many years and continues to be effective today.

Buying and selling real estate as an investment strategy is quite different from simply buying a home or commercial building. Just as important in determining FMV (fair market value) as comparable properties are when buying a home, the income stream generated by a property is a primary component for an investor. You typically have three options if you want to invest in real estate:

Buying and selling real estate as an investment strategy is quite different from simply buying a home or commercial building. Just as important in determining FMV (fair market value) as comparable properties are when buying a home, the income stream generated by a property is a primary component for an investor. You typically have three options if you want to invest in real estate:

Investing in FX (foreign exchange), currency speculation, and hedging are variations of the same basic investment strategy—you are betting that one currency will strengthen or weaken against the other. Not for the faint-hearted, these investments involve more due diligence and savvy than all of the other security types we have covered so far. Trading in FX is requires a strong macro-economic background and an understanding of interest rates as well.

Investing in FX (foreign exchange), currency speculation, and hedging are variations of the same basic investment strategy—you are betting that one currency will strengthen or weaken against the other. Not for the faint-hearted, these investments involve more due diligence and savvy than all of the other security types we have covered so far. Trading in FX is requires a strong macro-economic background and an understanding of interest rates as well.

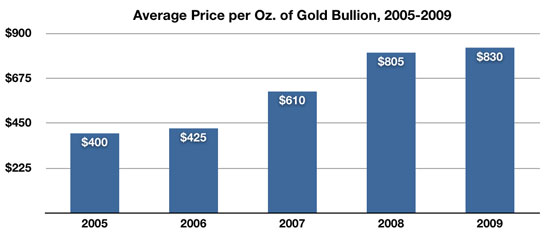

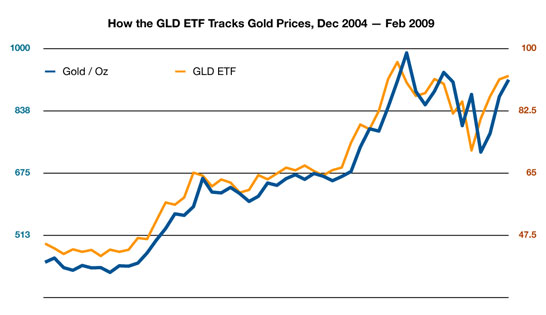

Precious metals, particularly gold and silver, are attractive investments to many people. But as usual, you must learn to become a knowledgeable investor as precious metals can fluctuate in value as rapidly as common

Precious metals, particularly gold and silver, are attractive investments to many people. But as usual, you must learn to become a knowledgeable investor as precious metals can fluctuate in value as rapidly as common

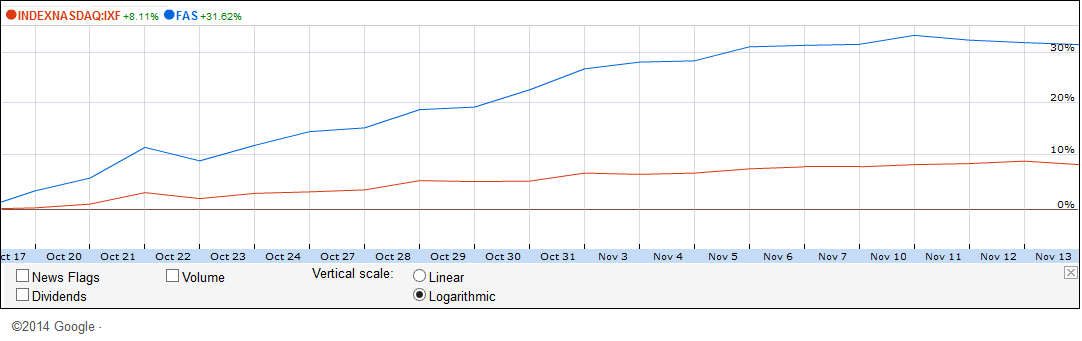

If you had invested in IXF in the summer of 2009, you would have done well, earning about 17% in one month. But if you had invested in FAS, you would have made a killing of over 70%! That is the power of leveraged ETFs. However, remember that leverage cuts both ways: up and down.

If you had invested in IXF in the summer of 2009, you would have done well, earning about 17% in one month. But if you had invested in FAS, you would have made a killing of over 70%! That is the power of leveraged ETFs. However, remember that leverage cuts both ways: up and down.